SLIDE 1

1

The Game: The Mover and The Follower in Stock Splits

Yasuharu Kuse and Seki Obata Keio Business School seki@kbs.keio.ac.jp kyasu@mbd.nifty.com

Very Preliminary. Please do not cite.

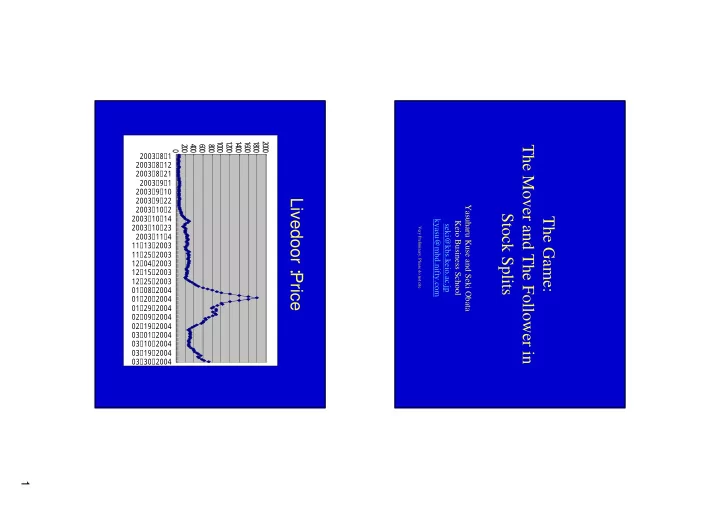

Livedoor: Price

2 4 6 8 1 1 2 1 4 1 6 1 8 2 2 3 / 8 / 1 2 3 / 8 / 1 2 2 3 / 8 / 2 1 2 3 / 9 / 1 2 3 / 9 / 1 2 3 / 9 / 2 2 2 3 / 1 / 2 2 3 / 1 / 1 4 2 3 / 1 / 2 3 2 3 / 1 1 / 4 1 1 / 1 3 / 2 3 1 1 / 2 5 / 2 3 1 2 / 4 / 2 3 1 2 / 1 5 / 2 3 1 2 / 2 5 / 2 3 1 / 8 / 2 4 1 / 2 / 2 4 1 / 2 9 / 2 4 2 / 9 / 2 4 2 / 1 9 / 2 4 3 / 1 / 2 4 3 / 1 / 2 4 3 / 1 9 / 2 4 3 / 3 / 2 4