SLIDE 1

The Economic Outlook TD Economics, April 2013

The Economic Outlook

Derek Burleton Vice President and Deputy Chief Economist

April 2013

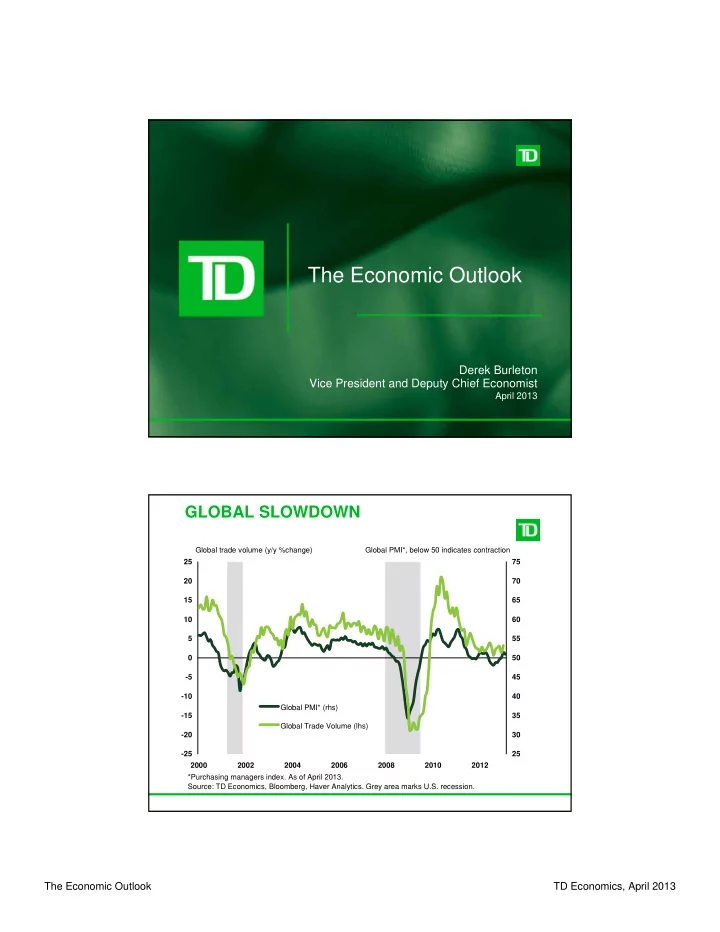

GLOBAL SLOWDOWN

- 25

- 20

- 15

- 10

- 5

5 10 15 20 25 2000 2002 2004 2006 2008 2010 2012 25 30 35 40 45 50 55 60 65 70 75 Global PMI* (rhs) Global Trade Volume (lhs) Global PMI*, below 50 indicates contraction Global trade volume (y/y %change) *Purchasing managers index. As of April 2013. Source: TD Economics, Bloomberg, Haver Analytics. Grey area marks U.S. recession.