SLIDE 1

Summary of Proposed Changes to Reporting Requirements Under Form 8-K

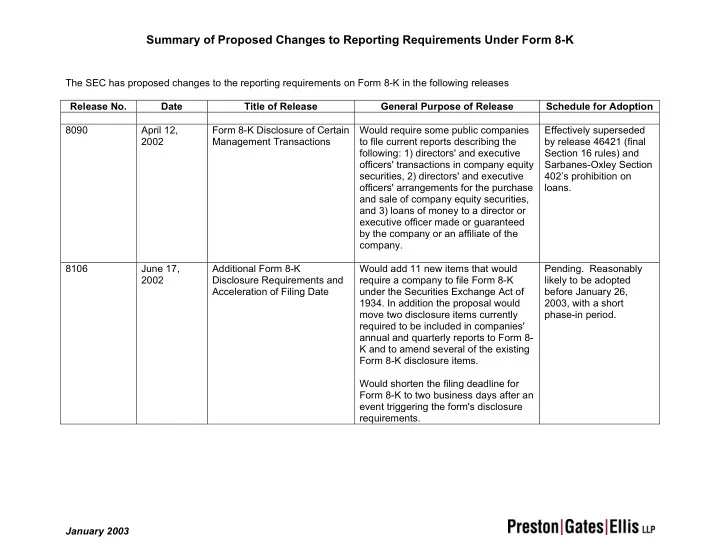

The SEC has proposed changes to the reporting requirements on Form 8-K in the following releases Release No. Date Title of Release General Purpose of Release Schedule for Adoption 8090 April 12, 2002 Form 8-K Disclosure of Certain Management Transactions Would require some public companies to file current reports describing the following: 1) directors' and executive

- fficers' transactions in company equity

securities, 2) directors' and executive

- fficers' arrangements for the purchase

and sale of company equity securities, and 3) loans of money to a director or executive officer made or guaranteed by the company or an affiliate of the company. Effectively superseded by release 46421 (final Section 16 rules) and Sarbanes-Oxley Section 402’s prohibition on loans. 8106 June 17, 2002 Additional Form 8-K Disclosure Requirements and Acceleration of Filing Date Would add 11 new items that would require a company to file Form 8-K under the Securities Exchange Act of

- 1934. In addition the proposal would

move two disclosure items currently required to be included in companies' annual and quarterly reports to Form 8- K and to amend several of the existing Form 8-K disclosure items. Would shorten the filing deadline for Form 8-K to two business days after an event triggering the form's disclosure requirements.

- Pending. Reasonably