SLIDE 1

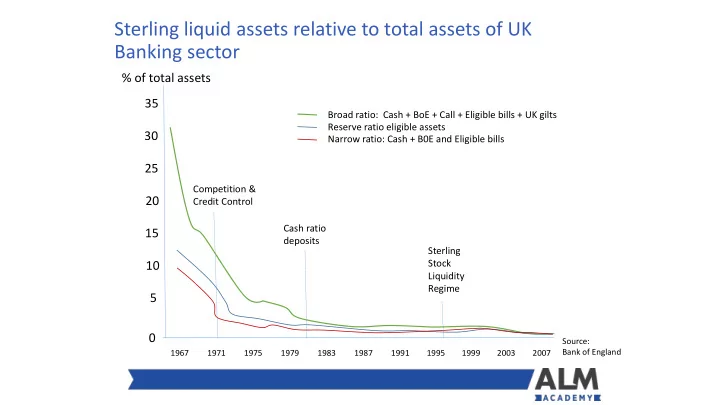

Sterling liquid assets relative to total assets of UK Banking sector

1967 1983 1975 1991 2007 1999 1987 1995 1979 2003 1971

30 15 20 25 10 5 35 % of total assets

Broad ratio: Cash + BoE + Call + Eligible bills + UK gilts Reserve ratio eligible assets Narrow ratio: Cash + B0E and Eligible bills Competition & Credit Control Cash ratio deposits Sterling Stock Liquidity Regime

Source: Bank of England