SLIDE 1 ¡ ¡

Brian ¡K. ¡Langenberg, ¡CFA ¡ ¡ ¡| ¡ ¡ ¡312.235.6521 ¡ ¡ ¡| ¡ ¡ ¡Brian@Langenberg-‑llc.com ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡1 ¡

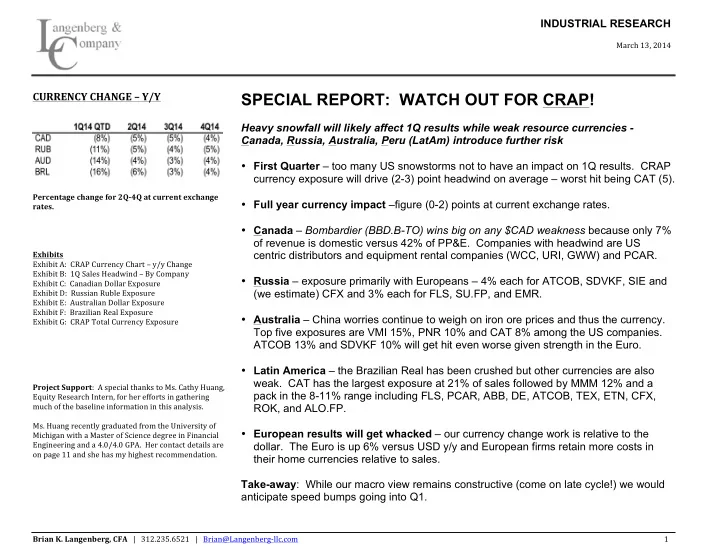

¡ CURRENCY ¡CHANGE ¡– ¡Y/Y ¡ ¡ ¡

Percentage ¡change ¡for ¡2Q-‑4Q ¡at ¡current ¡exchange ¡

¡ ¡ ¡

Exhibits ¡ Exhibit ¡A: ¡ ¡CRAP ¡Currency ¡Chart ¡– ¡y/y ¡Change ¡ Exhibit ¡B: ¡ ¡1Q ¡Sales ¡Headwind ¡– ¡By ¡Company ¡ Exhibit ¡C: ¡ ¡Canadian ¡Dollar ¡Exposure ¡ Exhibit ¡D: ¡ ¡Russian ¡Ruble ¡Exposure ¡ Exhibit ¡E: ¡ ¡Australian ¡Dollar ¡Exposure ¡ Exhibit ¡F: ¡ ¡Brazilian ¡Real ¡Exposure ¡ Exhibit ¡G: ¡ ¡CRAP ¡Total ¡Currency ¡Exposure ¡

¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ SPECIAL REPORT: WATCH OUT FOR CRAP! ¡ Heavy snowfall will likely affect 1Q results while weak resource currencies - Canada, Russia, Australia, Peru (LatAm) introduce further risk First Quarter – too many US snowstorms not to have an impact on 1Q results. CRAP currency exposure will drive (2-3) point headwind on average – worst hit being CAT (5). Full year currency impact –figure (0-2) points at current exchange rates. Canada – Bombardier (BBD.B-TO) wins big on any $CAD weakness because only 7%

- f revenue is domestic versus 42% of PP&E. Companies with headwind are US

centric distributors and equipment rental companies (WCC, URI, GWW) and PCAR. Russia – exposure primarily with Europeans – 4% each for ATCOB, SDVKF, SIE and (we estimate) CFX and 3% each for FLS, SU.FP, and EMR. Australia – China worries continue to weigh on iron ore prices and thus the currency. Top five exposures are VMI 15%, PNR 10% and CAT 8% among the US companies. ATCOB 13% and SDVKF 10% will get hit even worse given strength in the Euro. Latin America – the Brazilian Real has been crushed but other currencies are also

- weak. CAT has the largest exposure at 21% of sales followed by MMM 12% and a

pack in the 8-11% range including FLS, PCAR, ABB, DE, ATCOB, TEX, ETN, CFX, ROK, and ALO.FP. European results will get whacked – our currency change work is relative to the

- dollar. The Euro is up 6% versus USD y/y and European firms retain more costs in

their home currencies relative to sales. Take-away: While our macro view remains constructive (come on late cycle!) we would anticipate speed bumps going into Q1. ¡

Project ¡Support: ¡ ¡A ¡special ¡thanks ¡to ¡Ms. ¡Cathy ¡Huang, ¡ Equity ¡Research ¡Intern, ¡for ¡her ¡efforts ¡in ¡gathering ¡ much ¡of ¡the ¡baseline ¡information ¡in ¡this ¡analysis. ¡ ¡ ¡ ¡

- Ms. ¡Huang ¡recently ¡graduated ¡from ¡the ¡University ¡of ¡

Michigan ¡with ¡a ¡Master ¡of ¡Science ¡degree ¡in ¡Financial ¡ Engineering ¡and ¡a ¡4.0/4.0 ¡GPA. ¡ ¡Her ¡contact ¡details ¡are ¡

- n ¡page ¡11 ¡and ¡she ¡has ¡my ¡highest ¡recommendation. ¡

INDUSTRIAL RESEARCH

¡

March ¡13, ¡2014 ¡ ¡

SLIDE 2 ¡

Brian ¡K. ¡Langenberg, ¡CFA ¡ ¡ ¡| ¡ ¡ ¡312.235.6521 ¡ ¡ ¡| ¡ ¡ ¡Brian@Langenberg-‑llc.com ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡2 ¡

¡ ¡

WHY THIS REPORT: Investors are broadly aware of macro concerns and even currency – but we also believe there may be certain companies where the risk is underestimated or not fully understood, particularly with respect to Canada (Curling epicenter of the Universe!) but also Russia (12 of 46 actively monitored companies have currency exposure of 2-4% - not huge, but it matters). METHODOLOGY: This was not easy. During the Cold War currency impact was about the dollar, Deutschemark, and Yen – nothing else mattered. Also, Bond films were fun, the British Navy had more than 13 warships and Chairman Mao outfits were not yet considered chic. Times have changed. Now we have US, Canada, US and Canada, North America, Americas, Other Americas, Latin America + Canada, Brazil, and don’t even get me started on Europe, Western Europe, EMEA, MEA Europe and CIS (which includes Ukraine and Crimea). My point is that these exposures are, in many cases, estimates. Sources may include (in order of preference):

- 1. Corporate filings

- 2. Corporate slide decks

- 3. Corporate management

- 4. Trade articles quoting company executives

- 5. Data services

- 6. National economic data

- 7. Geopolitical judgment and likely trade flows

- 8. Where necessary, Powerful Secret Algorithms (PSA) were

- deployed. Which means I guessed.

One miscreant (actually, a great management team) provides 80%

- f revenue as “rest of world” – but analytically we don’t back down

from anything – and we studied presentations from acquisitions as far back as 2008 to derive an estimate of their geographic mix. Investors and executives are invited to call me to discuss methodology on a given company in more detail. STOCKS WITH HIGHEST 1Q REVENUE HEADWIND: We estimate that 25 of 46 studied companies will incur at least a two percentage point revenue headwind in the first quarter owing to weakness in one or more of the CRAP currencies – Canada, Russia, Australia or Latin America (Peru was used only to get the letter P – the analysis utilized the Brazilian Real though the Peruvian Peso is mining driven and also weak). Here are the top two “revenue” headwind names: Caterpillar (CAT) CRAP FX estimate: 36% 1Q sales headwind: (5%) 1Q Estimate, L30 days: No change CAT has worked out well – finally! – after we told clients beginning in mid-2013 that the low 80’s was an attractive entry point. The shares can easily trade to $110 or higher on China bullishness but the first quarter will be challenged by heavy exposure to Latin America at 21% of sales, Australia 8% and Canada 6%.

SLIDE 3 ¡

Brian ¡K. ¡Langenberg, ¡CFA ¡ ¡ ¡| ¡ ¡ ¡312.235.6521 ¡ ¡ ¡| ¡ ¡ ¡Brian@Langenberg-‑llc.com ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡3 ¡

¡

Atlas-Copco (ATCOB) CRAP FX estimate: 32% 1Q sales headwind: (4%) 1Q estimate, L30 days:

- 1Q Consensus is SEK 2.41 versus SEK2.67. Given that 4Q13

results were SEK 2.38 versus SEK 2.81 despite (4) points of currency headwind that seems realistic. Mining results have held up relatively well (i.e. – down less) because of a) greater aftermarket and services mix than others, b) strong management and c) execution around costs. Also – currency impact lessens after 1Q as the Australian dollar and Latin American currencies tanked between 1Q and 2Q in 2013. Other companies with (3) points of headwind include SDVKF, PCAR, FLS, PNR, ALO.FP, and DE.

SIGNIFICANT REVENUE / COST MISMATCHES We also reviewed each company for significant second derivative exposures owing to revenue / asset mismatches.

BBD.B-TO: Bombardier benefits from a weak $CAD as the local market currency is only 7% of sales but represents 42% of long-term cost structure. ERJ: Revenues are primarily USD, costs predominantly in Brazilian

- Real. Expect margin – excluding the vagaries of Brazilian

accounting – to benefit. ABB: This gets dicey. ABB’s functional currency is USD but its fixed plant is skewed toward Europe. And within that the Swiss Franc can loom large, as the home country is about 3% of sales but 19% of costs.

- Latin America is estimated at 17% of sales. Bad.

- Euro is up 6% versus USD y/y – and whereas the U.S. about

17% of ABB revenue the Euro represents about 42% of the long lived cost structure.

- Swiss Franc is up 1-2% versus the Euro or about 7-8%

versus the dollar and with the revenue / fixed cost mismatch can cause damage. IR: Using data from the 2013 10-K the US represents 59% of revenue, 80% of long-lived assets. XYL: Europe 35% of sales, 45% of PP&E. Much or that entire gap is the Swedish Krona, which is, fortunately for Xylem, down about (5%) versus the Euro year over year. MMM: US 36% of sales, 52% of PP&E. 3M Company has fairly sizable revenue to costs mismatch and with relatively large Latin America exposure (we estimate 12% of sales) faces a headwind.

SLIDE 4

¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ Exhibit A: CRAP Currency – y/y Change ¡

Brian ¡K. ¡Langenberg, ¡CFA ¡ ¡ ¡| ¡ ¡ ¡312.235.6521 ¡ ¡ ¡| ¡ ¡ ¡Brian@Langenberg-‑llc.com ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡4 ¡

¡ ¡ ¡ ¡ ¡

SLIDE 5

¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ Exhibit B: 2+ Points 1Q Sales Headwind ¡

Brian ¡K. ¡Langenberg, ¡CFA ¡ ¡ ¡| ¡ ¡ ¡312.235.6521 ¡ ¡ ¡| ¡ ¡ ¡Brian@Langenberg-‑llc.com ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡5 ¡

¡ ¡

SLIDE 6

¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡Exhibit C: Canada ¡

Brian ¡K. ¡Langenberg, ¡CFA ¡ ¡ ¡| ¡ ¡ ¡312.235.6521 ¡ ¡ ¡| ¡ ¡ ¡Brian@Langenberg-‑llc.com ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡6 ¡

¡ ¡ ¡ ¡ ¡

SLIDE 7

¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡Exhibit D: Russia ¡

Brian ¡K. ¡Langenberg, ¡CFA ¡ ¡ ¡| ¡ ¡ ¡312.235.6521 ¡ ¡ ¡| ¡ ¡ ¡Brian@Langenberg-‑llc.com ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡7 ¡

¡ ¡ ¡ ¡ ¡ ¡

SLIDE 8

¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡Exhibit E: Australia ¡

Brian ¡K. ¡Langenberg, ¡CFA ¡ ¡ ¡| ¡ ¡ ¡312.235.6521 ¡ ¡ ¡| ¡ ¡ ¡Brian@Langenberg-‑llc.com ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡8 ¡

¡ ¡ ¡ ¡ ¡

SLIDE 9

¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡Exhibit F: Latin America ¡

Brian ¡K. ¡Langenberg, ¡CFA ¡ ¡ ¡| ¡ ¡ ¡312.235.6521 ¡ ¡ ¡| ¡ ¡ ¡Brian@Langenberg-‑llc.com ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡9 ¡

¡ ¡ ¡ ¡ ¡

SLIDE 10

¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡Exhibit G: CRAP Total Exposure ¡

Brian ¡K. ¡Langenberg, ¡CFA ¡ ¡ ¡| ¡ ¡ ¡312.235.6521 ¡ ¡ ¡| ¡ ¡ ¡Brian@Langenberg-‑llc.com ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡10 ¡

¡

SLIDE 11 ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡Disclosures, Disclaimer ¡

Brian ¡K. ¡Langenberg, ¡CFA ¡ ¡ ¡| ¡ ¡ ¡312.235.6521 ¡ ¡ ¡| ¡ ¡ ¡Brian@Langenberg-‑llc.com ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡11 ¡

¡ Research ¡Leadership ¡ ¡

Brian ¡K. ¡Langenberg, ¡CFA ¡ Principal ¡ ¡ Director ¡of ¡Research ¡ ¡ 312.235.6521 ¡ Brian@Langenberg-‑llc.com ¡

¡ ¡ ¡

Nathan ¡E. ¡Yates ¡ Research ¡Associate ¡ ¡ 312.802.6393 ¡ Nathan@Langenberg-‑llc.com ¡

¡ ¡

- Ms. ¡Fan ¡(Cathy) ¡Huang ¡

Equity ¡Research ¡Intern ¡ 734.604.7076 ¡ fhua@umich.edu ¡

¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ ¡ Disclosures ¡

¡ Rating ¡System: ¡ ¡We ¡refer ¡to ¡multiple ¡target ¡prices ¡on ¡each ¡security, ¡reflecting ¡time ¡(3 ¡year, ¡1 ¡year, ¡occasionally ¡near ¡ term), ¡and ¡various ¡scenarios ¡as ¡well ¡as ¡relative ¡recommendations ¡between ¡two ¡or ¡more ¡securities. ¡ ¡ Analyst ¡Certification: ¡ ¡I, ¡Brian ¡K. ¡Langenberg, ¡CFA, ¡certify ¡that ¡the ¡views ¡expressed ¡in ¡this ¡publication ¡accurately ¡ reflect ¡my ¡personal ¡views ¡about ¡the ¡subject ¡companies ¡and ¡their ¡securities. ¡ ¡I ¡also ¡certify ¡that ¡I ¡have ¡not, ¡am ¡not, ¡and ¡ will ¡not ¡be ¡compensated ¡directly ¡or ¡indirectly ¡in ¡exchange ¡for ¡expressing ¡any ¡specific ¡recommendation ¡in ¡this ¡report. ¡ ¡ Required ¡Disclosures: ¡ ¡Brian ¡K. ¡Langenberg, ¡CFA ¡may ¡or ¡may ¡not ¡own ¡long ¡or ¡short ¡positions ¡in ¡securities ¡mentioned ¡ in ¡this ¡report. ¡ ¡As ¡a ¡matter ¡of ¡principal ¡and ¡ethics, ¡neither ¡he ¡nor ¡Langenberg ¡& ¡Company ¡employees ¡will ¡trade ¡for ¡three ¡ days ¡in ¡any ¡security ¡expected ¡to ¡be ¡mentioned ¡in ¡any ¡report. ¡ ¡Occasionally, ¡the ¡time ¡gap ¡between ¡a ¡personal ¡trade ¡and ¡ an ¡unanticipated ¡event ¡may ¡be ¡less. ¡ ¡There ¡is ¡no ¡known ¡affiliate ¡ownership ¡in ¡subject ¡companies ¡of ¡this ¡report. ¡ ¡ ¡No ¡ known ¡Langenberg ¡& ¡Company, ¡LLC ¡employee, ¡officer, ¡or ¡affiliate ¡serves ¡as ¡an ¡officer, ¡director, ¡or ¡advisory ¡board ¡ member ¡of ¡subject ¡companies ¡in ¡this ¡report. ¡ ¡The ¡firm ¡does ¡seek ¡to ¡sell ¡research ¡descriptions ¡to ¡industrial ¡companies ¡ including ¡those ¡mentioned ¡in ¡this ¡report. ¡ ¡No ¡other ¡known ¡conflicts ¡exist. ¡ ¡ Important ¡Disclosures: ¡ ¡Langenberg ¡& ¡Company, ¡LLC ¡(L&C) ¡employs ¡various ¡equity ¡valuation ¡methodologies ¡ including ¡free ¡cash ¡flow ¡yield, ¡price/earnings ¡(P/E), ¡and ¡enterprise ¡value/EBITDA, ¡among ¡others ¡regarding ¡investment ¡ ratings, ¡target ¡prices ¡and ¡conclusions. ¡ ¡Certain ¡risks ¡to ¡our ¡ratings, ¡target ¡prices ¡and ¡ultimate ¡investment ¡conclusions ¡ exist ¡which ¡include, ¡without ¡limitation, ¡a ¡company’s ¡failure ¡to ¡achieve ¡financial ¡results, ¡product ¡risk, ¡regulatory ¡risk, ¡ general ¡market ¡conditions ¡and ¡volatility, ¡interest ¡rates, ¡political ¡factors, ¡acts ¡of ¡God, ¡terrorist ¡activities ¡and ¡changing ¡ economic ¡conditions. ¡ ¡L&C ¡is ¡not ¡a ¡registered ¡investment ¡advisor ¡and ¡is ¡not ¡acting ¡as ¡a ¡broker ¡dealer ¡under ¡any ¡federal ¡

- r ¡state ¡securities ¡laws. ¡ ¡Notable ¡compliance ¡policies ¡include ¡(1) ¡prohibition ¡of ¡insider ¡trading ¡or ¡the ¡facilitation ¡

thereof, ¡(2) ¡maintaining ¡client ¡confidentiality, ¡(3) ¡archival ¡of ¡electronic ¡communications, ¡and ¡(4) ¡appropriate ¡uses ¡of ¡ electronic ¡communications, ¡amongst ¡other ¡compliance ¡related ¡policies. ¡

¡ Disclaimer ¡

Material ¡provided ¡in ¡this ¡publication ¡is ¡for ¡general ¡informational ¡purposes ¡only, ¡and ¡was ¡prepared ¡from ¡sources ¡and ¡ data ¡believed ¡to ¡be ¡reliable, ¡but ¡we ¡do ¡not ¡guarantee ¡its ¡accuracy ¡or ¡completeness. ¡ ¡We ¡cannot ¡and ¡do ¡not ¡guarantee ¡the ¡ adequacy, ¡accuracy ¡or ¡completeness ¡of ¡this ¡information ¡or ¡the ¡suitability ¡or ¡profitability ¡of ¡any ¡particular ¡investment. ¡ ¡ This ¡publication ¡does ¡not ¡consider ¡the ¡specific ¡investment ¡objectives, ¡financial ¡situation, ¡or ¡particular ¡needs ¡of ¡any ¡ specific ¡person, ¡or ¡any ¡investment ¡laws ¡and ¡regulations, ¡regulatory ¡capital ¡requirements, ¡or ¡other ¡restriction ¡ applicable ¡to ¡investments ¡by ¡certain ¡institutional ¡investors. ¡ ¡Accordingly, ¡you ¡are ¡responsible ¡for ¡your ¡own ¡investment ¡ research ¡and ¡decisions, ¡and ¡should ¡seek ¡the ¡advice ¡of ¡a ¡qualified ¡fiduciary, ¡and ¡perform ¡your ¡own ¡due ¡diligence ¡before ¡

- investing. ¡ ¡You ¡should ¡also ¡consult ¡your ¡own ¡legal ¡advisor ¡in ¡determining ¡the ¡legality ¡and ¡consequences ¡to ¡you ¡of ¡the ¡

purchase, ¡ownership, ¡or ¡sale ¡of ¡any ¡investments. ¡ ¡ No ¡information ¡in ¡this ¡or ¡any ¡of ¡our ¡publications ¡is ¡intended ¡as ¡tax, ¡accounting, ¡or ¡legal ¡advice, ¡as ¡an ¡offer ¡or ¡ solicitation ¡of ¡an ¡offer ¡to ¡sell ¡or ¡buy, ¡or ¡as ¡a ¡sponsorship ¡of ¡any ¡company, ¡security ¡or ¡fund. ¡ ¡Past ¡performance ¡does ¡not ¡ indicate ¡or ¡guarantee ¡future ¡performance ¡and ¡no ¡representation ¡or ¡warranty ¡is ¡made ¡regarding ¡future ¡performance. ¡ ¡ This ¡publication ¡reflects ¡a ¡judgment ¡at ¡its ¡original ¡date ¡of ¡publication ¡by ¡Langenberg ¡& ¡Company, ¡LLC ¡and ¡is ¡subject ¡to ¡ change ¡without ¡notice. ¡ ¡The ¡price, ¡value, ¡and ¡income ¡from ¡any ¡securities ¡or ¡instruments ¡mentioned ¡in ¡this ¡report ¡can ¡ fall ¡as ¡well ¡as ¡rise ¡as ¡a ¡result ¡of ¡a ¡host ¡of ¡factors ¡including, ¡but ¡not ¡limited ¡to, ¡economic, ¡financial, ¡and ¡political ¡factors, ¡ interest ¡rates, ¡stock ¡market ¡volatility, ¡commodity ¡price ¡and ¡exchange ¡rate ¡movements, ¡weather, ¡regulatory ¡changes, ¡ changes ¡in ¡credit ¡quality, ¡acts ¡of ¡God, ¡or ¡terrorist ¡activities. ¡

¡