SLIDE 1

One-step Binary Model (continued) Risk-Neutral Probability Measure

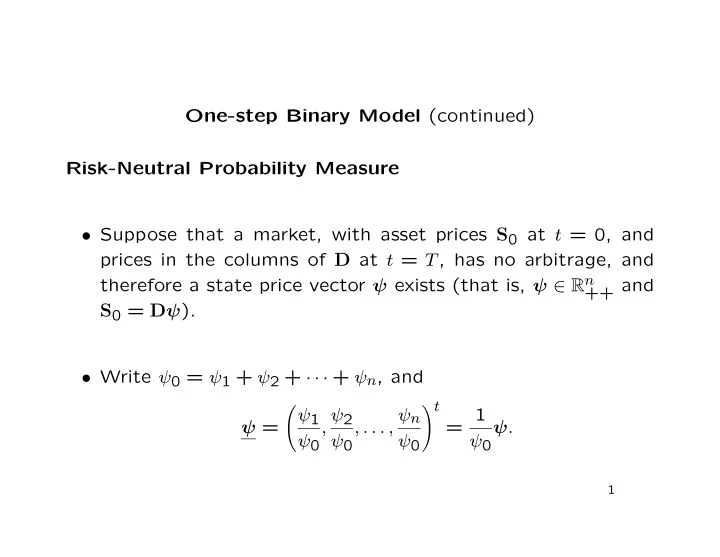

- Suppose that a market, with asset prices S0 at t = 0, and

prices in the columns of D at t = T, has no arbitrage, and therefore a state price vector ψ exists (that is, ψ ∈ Rn

++ and

S0 = Dψ).

- Write ψ0 = ψ1 + ψ2 + · · · + ψn, and

ψ =

- ψ1