1E ~~

cf5Iqx ~ HINDUSTAN COPPER LIMITED

C IN N o. : L 27201W B 1967G O I028825~~Jlm"r~

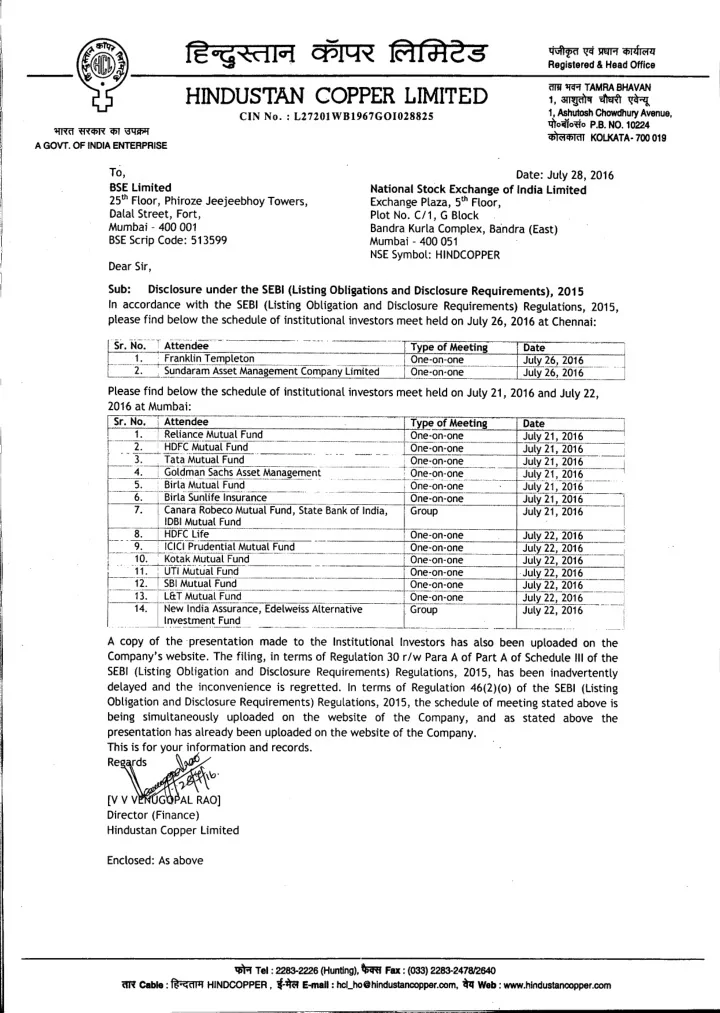

Registered & Head Office 0J1l''Jfq.J TAMRA BHAVAN 1,~~~ 1, Ashutosh Chowdhury Avenue, tIToiITo~o P.B. N O . 10224 q)~C1q;ltll KOLKATA. 700 019 To, BSE Limited 25th Floor, Phiroze Jeejeebhoy Towers, Dalal Street, Fort, Mumbai - 400 001 BSEScrip Code: 513599 Dear Sir, Date: July 28, 2016 National Stock Exchange of India Limited Exchange Plaza, 5th Floor, Plot No. C/1, G Block Bandra Kurla Complex, Bandra (East) Mumbai - 400 051 NSESymbol: HINDCOPPER Sub: Disclosure under the SEBI (Listing Obligations and Disclosure Requirements), 2015 In accordance with the SEBI (Listing Obligation and Disclosure Requirements) Regulations, 2015, please find below the schedule of institutional investors meet held on July 26, 2016 at Chennai:r-~~:-~1:~:~I~~;~~~~;~~~~==:::: .•.

- ...._____

L~~~~~~~~;:~i~_~ __~l~?~?~1~_

_ _,

L.__ ._~_--' .. 2~_l1daram A ssetM ?na~em en_t~~!:!:e..any ~im it~_J_()~t:::£ll1-o~____ July 26,-20~ _ Please find below the schedule of institutional investors meet held on July 21, 2016 and July 22, 2016 at Mumbai:pr~~. '.

'~~~~~~:e~utU :~F~~-;-----------.~"---~~()~~o~:eting D ate-

r- ..---2:-.:.--H D F-e-M utualFun-a-.--..- ..

- -.----

..

- --.--fO ne-6i1=-6i1e-------

.~~~~ ~}~~~ ~------

l~~~~4~~~j:~~1~~~~~~~~~~!-¥~~i~~j15int

- L£6~~~~:~~~-------~~~_~+.~lt=::-j

5. B irlaM utualFund , O ne-on-one July 21,2016 :=--6:-::'=_~jrl~ Sun1ife-T nsurance---~_=_~-===T -O ne:6n-o~-=----" J~y 21,2016-

=:

7. ,C anara R obecoM utualFund, State B ankof India,

! G roupJuly 21, 2016 . lO B I M utualFund

I

- - ...

a.---rH tW cille----------------

- ..----------rO ne-on-one---

July 2i~1016-

..

- -...

....,

. ?~

I~l~_I.:J:lr~_~~~i?!J\'\l,l~~lf.lJn~____ . _ .__ L 911~:9~:~t:______ July 22, 2016

i .- .1L ~~la_~J\'\~tual

Fund ._

! O ne-on-oneJulyii~i016--------i

I-----H -~_.

~~I~~fG ig~~g-------------------+g~-~*~:6~:- j~:~~~: ;~~:

.- _-- .---

- .-

- .-.--.--

- ..

- ..

- ..-----

- .-

- _._

13. : L&T M utualFund

i O ne-on-oneJuly 22,2016

- ------~~T~;;:~~~~;~~~~_

E d:I::ssA fter~a_t~_~~~=~[~:u~-~:==-_~~=:~' J~~_~~~2016- A copy of the presentation made to the Institutional Investors has also been uploaded

- n the

- f the

- n

- f

- HINDCOPPER. t.~