SLIDE 1

1

Interim Report

April-June 2015

Johan Dennelind, President & CEO

Q2

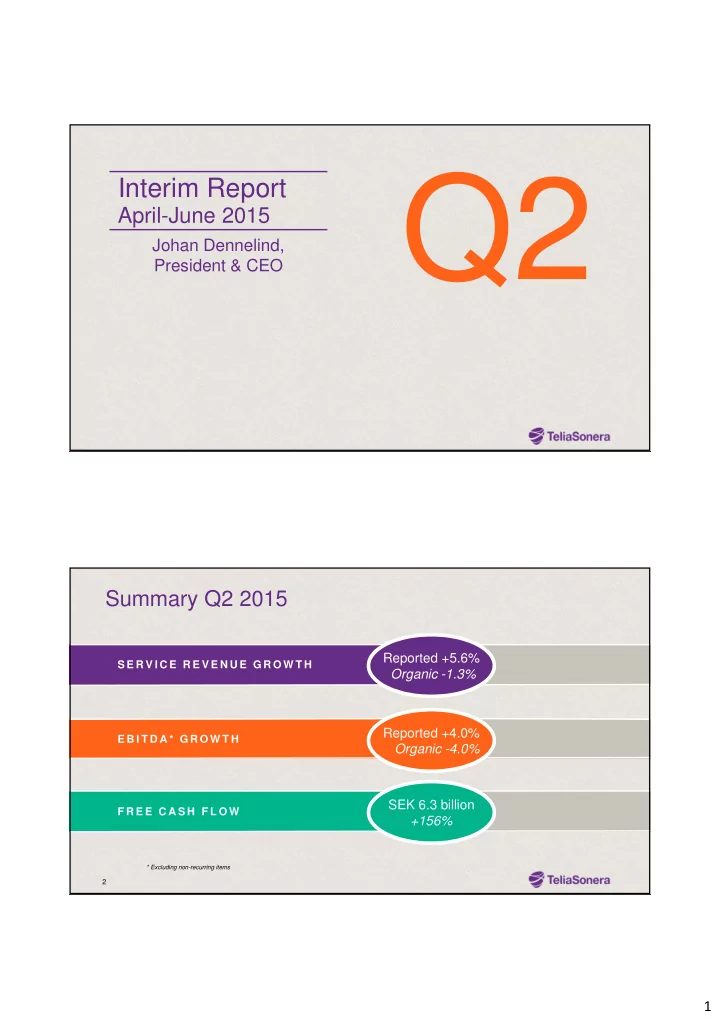

*Summary Q2 2015

2 S E R V I C E R E V E N U E G R O W T H E B I T D A * G R O W T H F R E E C A S H F L O WReported +5.6% Organic -1.3% Reported +4.0% Organic -4.0% SEK 6.3 billion +156%

* Excluding non-recurring items