Inequality and Development – Week 10 March 12

Readings: Ray chapter 7 Ray chapter 7 Benabou & Mookherjee chapter 4 and 12

1

Questions that we will discuss today

T k hi i ll i i i i l di ib i f b h

- Take historically given an initial distribution of assets, but then

ask the question: Do inequalities worsen or narrow with economic development? How are aggregates, such as income, wealth, savings, and growth rates affected by inequality? In turn, how do these variables affect the evolution of inequality?

2

Outline of the lecture Outline of the lecture

E i i l tt b t i lit d i d l t/i Empirical pattern between inequality and economic development/income. The inverted-U hypothesis From inequality to aggregates Inequality → savings. Inequality → growth Inequality → growth. Inequality → credit constraints. Inequality → occupational choice.

Inequality → savings → Inequality Inequality → credit constraints → Inequality Inequality → occupational choice → Inequality Inequality → growth → Inequality

From aggregates to inequality Savings → Inequality Growth → Inequality. Credit constraints → Inequality. Occupational choice → Inequality. p q y

3

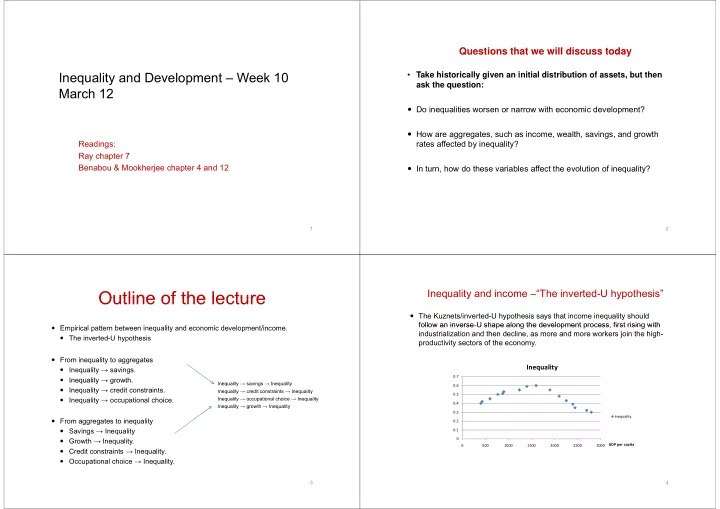

Inequality and income –“The inverted-U hypothesis” q y yp

The Kuznets/inverted-U hypothesis says that income inequality should follow an inverse-U shape along the development process first rising with follow an inverse U shape along the development process, first rising with industrialization and then decline, as more and more workers join the high- productivity sectors of the economy.

0.7

Inequality

0.4 0.5 0.6 0.1 0.2 0.3 inequality 500 1000 1500 2000 2500 3000 GDP per capita

4