SLIDE 1

Microinsurance Conference in Munich 18-20 October 2005

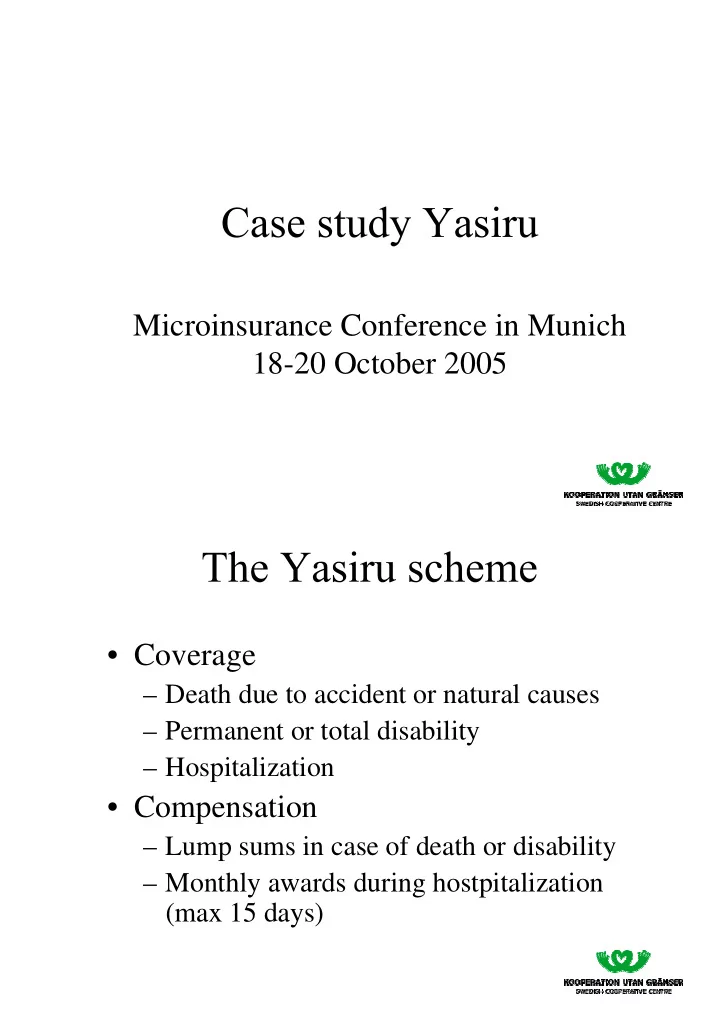

- Coverage

– Death due to accident or natural causes – Permanent or total disability – Hospitalization

- Compensation

Microinsurance Conference in Munich 18-20 October 2005 Coverage - - PDF document

Microinsurance Conference in Munich 18-20 October 2005 Coverage Death due to accident or natural causes Permanent or total disability Hospitalization Compensation Lump sums in case of death or disability Monthly