SLIDE 1

Insurance and Indemnification by Charles Spencer, County of Volusia Risk Manager

Page 1 of 9 History of insurance – Lloyd’s What does a commercial insurance policy look like?

- Do insurance companies draft their own insurance policy that they sell?

- What is ISO (Insurance Services Office) and what does it do?

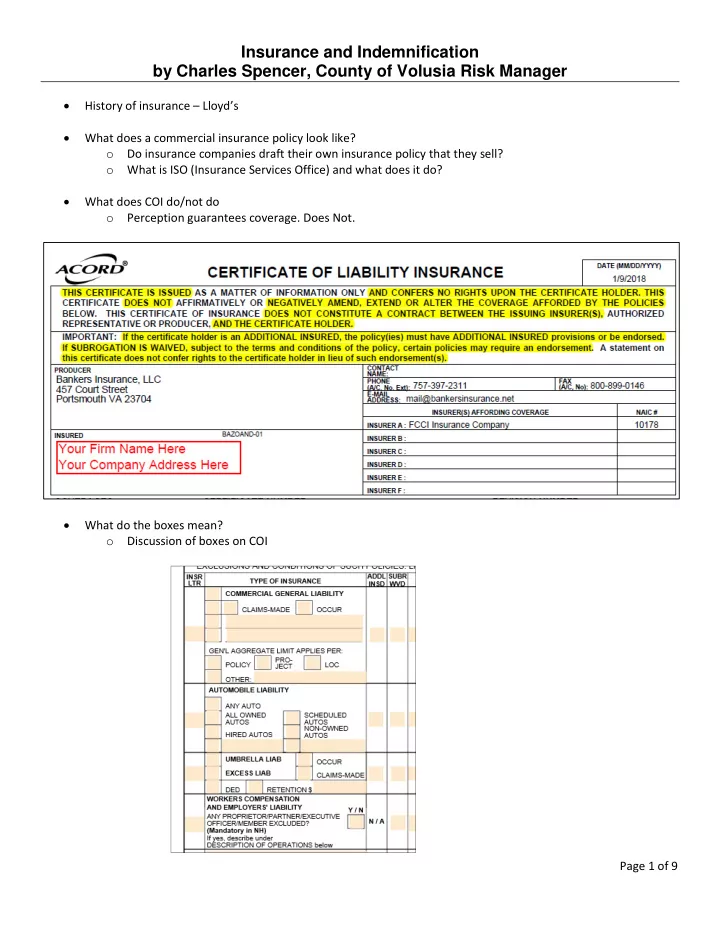

What does COI do/not do

- Perception guarantees coverage. Does Not.

What do the boxes mean?

- Discussion of boxes on COI