SLIDE 1

High Purity Quartz Pty Ltd Company Presentation Equity Issue - - PowerPoint PPT Presentation

High Purity Quartz Pty Ltd Company Presentation Equity Issue November 2016 0 Important Notice This document is confidential and its content may not be copied, reproduced, redistributed, quoted, referred to or otherwise disclosed, in whole

1

Important Notice

This document is confidential and its content may not be copied, reproduced, redistributed, quoted, referred to or

High Purity Quartz Pty Ltd (“the Company” or “HPQM”). This document is for informational purposes only, and does not constitute or form part of an offer, solicitation or invitation of any offer, to buy or subscribe for any securities, nor should it or any part of it form the basis of, or be relied in any connection with, any contract or commitment whatsoever. Any invitation to subscribe for securities in the Company will be subject to a formal document. This document contains interpretations and forward-looking statements that are subject to risk factors associated with the mining and processing industries. You are cautioned not to place reliance on these forward-looking statements, which are based on the current view of the Company on future events. Investing in securities is risky and investors are advised to seek their own advice in this regard. Investors should undertake their own investigations on potential qualification and availability of any investment tax incentives. The Company believes that the expectations reflected in the document are reasonable but may be affected by a variety of variables and changes in underlying assumptions which could cause actual results to differ substantially from the statements made. These include but are not limited to: production fluctuations, commodity price fluctuations, variations to drilling, resource estimates, loss of market, industry competition, environmental risk, physical risks, legislative fiscal and regulatory changes, changes to licences/regimes, economic and financial market conditions, project delay or advancement, approvals and cost estimates. The Company and its Advisors and their Directors, agents, officers or employees do not make any representation or warranty, express or implied, as to endorsement of, the fairness, accuracy or completeness of any information, statement, representation or forecast contained in this document and they do not accept any liability for any statement made in, or omitted from, this document. The information contained in this document noted above are subject to change without notice. This document is intended only for the recipients thereof and may not be forwarded or distributed to any other person and may not be copied or reproduced in any manner.

2

works to de-risk its high purity quartz resource to underpin its innovative High Purity Sand project. This initial work primarily involves a drilling & sampling program with associated assay/test work

through to planned IPO targeted for c12 months to fully fund its high purity sand project

de-risk the resource and related costs. See slide 31 for detail

HPQM at a valuation of cA$5m.

representing minimum 2,322 shares. There is no limit to the number of shares which an individual investor may subscribe

HPQM discretion. Final allocations, based on valid Application Forms received, will be notified in writing and will require completion of the final Subscription Agreement

HPQM by contacting one of the persons listed at the end of this presentation

Subject to satisfaction of certain conditions and subject to investor status any investment made may qualify for Early Stage Innovation Company (ESIC) incentives with advantageous Australian Income Tax and CGT incentives for investors (see Slide 33 for more detail)

3

HPQM currently has 418,000 shares on issue, and will issue 46,450 new shares to bring the total shares on issue to 464,450 shares. The new issue will represent 10.01% of the share capital. This will raise A$532,000 at A$11.45 per share. The proposed structure is provided by way of illustration and allows flexibility for potential future asset acquisitions/disposals and corporate development. The structure is therefore indicative only but is in line with HPQM business plan.

4

Renewable energy (solar PV) and semiconductor supply chain focus

Excellent Project Economics

Project Pathway established and investment de-risked

Near term exits and IPO potential

expressed interest.

5

6

Polysilicon metal (Si) is then melted and drawn into cylindrical ingots (boules). These ingots are wafered and are the basis of solar PV cells and semiconductor wafers

With huge growth in Solar PV energy and Semiconductor industries, security of high purity sand supply is now a key issue. Analogous to Lithium and battery storage markets

Polysilicon metal (Si) is loaded into CZ crucibles (Si02)

High Purity Sand is then sold to manufacturers of Czochralski (CZ) crucibles. The most efficient solar cells and semiconductors are made with CZ crucibles.

7

There are few producing resources - economic sources of chemically pure quartz is rare globally. New entrants will be limited. Downstream PV market needs a new entrant to secure growth.

8

9

10

downside 10%) and existing capacity renewal

13.1% to 20252

HPQ Materials plans to ease into the supply gap without oversupplying the market. Target market share of 10% to 15% once fully ramped-up over 5 years.

11

Resource Quality and Quantity

purity silica production

specific quartz resource

Technical Expertise and Know-How

benefication

through to product delivery and downstream manufacture

Processing

12

13

ØFully permitted mining lease in Australia. Outcropping quartz resource over 800m ridge Ø99.99% pure quartz in situ confirmed via independent NATA accredited laboratory assay ØInitial independent geologist review estimates circa 2 to 4 million tonnes (Note 1) on a pre-drilling, volumetric assessment basis assuming depths of 50m and 100m respectively. ØProvides mine life of 20-40 years (Note 1). ØSimple surface scree excavation followed by later drill and blast of outcropping resource ie Quarrying

Note 1 – these volumes are pre-drilling estimates. Volumes can only be ascertained with greater degree of certainty following the drilling program anticipated in the development plan. The mine life is estimated by dividing the estimated resource volume by the annual targeted ROM volume of c100k tonnes per annum.

14

Independent geologist report – 20 years mine life to 50 metres depth (4Mt to 100m) The initial drilling anticipated by this raising will confirm that quartz exists at depth. Volumes will only be known more fully after in-fill drilling scheduled for a later funding round.

Independent geologist resource estimates (n.b. non-JORC)

15

Al Fe Ca K Na Li SUM % SBH1 46.527 6.223 4.488 13.798 10.768 0.442 82.246 99.992 SBH2 50.680 15.717 2.562 23.977 10.007 0.753 103.696 99.990 SBH3 47.207 26.917 1.647 24.010 4.377 0.494 104.652 99.990 SBH4 72.005 45.958 1.526 100.434 5.246 0.405 225.574 99.977 SBH5 28.451 28.737 0.933 69.605 6.994 0.390 135.110 99.986 SBH6 31.889 4.743 3.613 17.198 13.959 0.396 71.798 99.993 SBH7 28.890 14.538 1.132 48.310 6.494 0.231 99.595 99.990 SBH8 40.650 9.520 2.668 27.553 10.498 0.224 91.113 99.991 SBH9 58.191 11.741 8.642 37.881 33.754 0.160 150.369 99.985 SBH10 46.289 11.487 1.255 36.542 3.224 0.202 98.999 99.990 AVERAGE 45.078 17.558 2.847 39.931 10.532 0.370 118.764 99.988

16

Raw material

HP5

manufacture.

HP7

polysilicon wafer/cell production and quartzware for solar PV manufacturers.

HP9

crucibles for polysilicon wafer production for electronic grade quartzware.

HPQM quartz resource is 99.99% pure in situ. This means that it can be potentially processed to higher grades (HP7 and HP9) economically

17

HP5 (Powder) HP5 (Sand) HP7 (Sand) HP9 (Sand)

Purity

99.99% 99.99% 99.997% 99.999%

Product Specification Total impurities: <100ppm Total impurities: <100ppm Total impurities: <30ppm Total impurities: <10ppm Markets High Purity Filler, specialty glass/ceramics, and Epoxy Molding Compounds Halogen and mercury lamps, custom production applications such as fused quartz tubing, and ingots Mono-crystalline crucibles, high grade multi-crystalline crucibles, high quality fused glass tubing and quartzware Semiconductor grade crucibles and high end solar and semiconductor applications Market Driver Consumer electronics, pharmaceutical packaging, high efficiency lighting. Solar PV equipment – CAGR 20-30% Semi-conductor equipment – CAGR 5-10%. Key Product Features By-product of higher grade processing High purity silica sand for fused quartz uses. Very high purity silica sand suitable for solar grade quartz crucibles and quartzware products Ultra high purity quartz sand suitable for semiconductor grade crucibles and quartzware products

Market Price USD/tonne (Estimated) $500-$1,000 $600-$1,500 $5,500-$8,500 $12,000-$15,000

HPQM will produce and market a range of high value products

18

19

Strong EBITDA growth, early cashflow , high value products – exceptional returns

Profit & Loss 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 $Am 1 2 3 4 5 6 7 8 9 10 Revenue 0.1 14.3 71.5 127.7 236.7 299.6 307.1 314.7 322.6 330.7 EBITDA (1.2) 0.9 37.5 87.2 176.7 227.8 234.2 240.0 245.9 251.9

6% 52% 68% 75% 76% 76% 76% 76% 76%

Earnings in Year (1.3) (1.5) 23.6 57.3 118.7 153.6 159.0 164.4 167.9 172.1

Sales Pricing

A$/tonne

HP5

1,450

HP5 Blend

500

HP5 - EMC

750

HP5 - HPF

750

HP7

8,000

HP9

12,000

20 Year Project NPV Discount Rate: 10% 20% NPV Cash (Pre-tax) 1,355,104 600,102 NPV Cash (Post-tax) 926,345 403,275 20 Year Project IRR Pre Tax 150% Post Tax 120%

EBITDA positive in second half of Year2 Low grade sales (HP Blend) starts in Month 6 Commercial cashflow (HP5) starts in Month 10 Early breakeven and payback

20

Valuation grows as incremental milestones achieved and project is de-risked DCF valuation based on milestone achievement and related reduction of risk discount Exit at significant multiple in 12 months via IPO is targeted

21

22

Phase 1a - A$3m Month 1-4

Phase 1b - A$5m Month 2-12

Phase 2a - A$30m Month 12 to 18

HPQM has adopted a staged development approach to mitigate development and investor risk.

Overall Funding Plan – Total A$38m Based on Development Milestones

Round 1a - A$3m Round 1b - A$5m Round 2 – A$30m

Note capex estimates for Phase 2 above are approximate and require finalization of materials testing and assessment Phase 1a can be further spilt as follows: Initial resource de-risking–drilling/testing to depth – cA$510k Asset acquisition, deliver low grade sales and high grade lab samples – cA$2.5m This equity raising

23

next round funders)

later rounds Appraisal drilling

Testing

Initial Mining for samples testing

rental and develop next round funding Staff/ Working capital and next funding round costs

Lease Maintenance Costs

HPQM is now seeking cA$510k to de-risk asset volumes through drilling and testing.

24

25

IPO

Compliance Listing

to secure supply to protect US$Billions invested Strategic Buy-Out

Trade Sale

Ø HPQM plans to IPO the business after Phase 1a and Phase 1b are completed Ø IPO will fund Phase 2 development Ø Strategic buy-out or trade sale is possible once asset de-risked and HP7 has been proven to pilot sample level

26

Initial raise opens up significant liquidity from large investors through to IPO.

sampling program

metallurgy

program

Asset/HP5 De-risking

HP5 Plant Construction/HP7 Pilot HP5 Production and Sales Ramp Up HP7 Plant Construction HP7 Production and Sales Ramp Up Round 1a Balance Raise $2.5m Feb 2017 IPO c$30m Nov 2017 Round 1b Raise $5.0m April 2016

Round 1a De-risk Raise $0.5m Nov/Dec 2016

Phase 1a (Balance raise $2.5m) + Phase 1b Raise ($5m) may be combined as a single $7.5m raise depending on results of initial de-risking works.

27

Stuart Jones – Chief Executive Officer

international banking

international operations and early stage project developments.

Jason May - Chief Technical Officer

Brook Burke - Company Secretary and General Counsel

public energy and resource companies

Queensland Andrew Hamilton – Chief Commercial Officer

and Resource sectors.

and exploration, operations management and logistics.

Experienced and dedicated management team covering all necessary disciplines ü Commercial ü Financial ü Technical ü Sales & Marketing ü Operational ü Legal ü Risk ü Compliance ü International

28

29

The market needs a new long term supplier of one of the world’s most strategic mineral. ØHigh Purity Quartz Sand is the only material suitable for high purity quartz crucible manufacture ØQuartz crucibles are used as the melting pots to produce both mono-crystalline and multi-crystalline polysilicon ØMono-crystalline solar PV cells produce higher energy output per cell than multi-crystalline cells ØConsequently, mono-crystalline polysilicon is growing its share of the solar PV cell/wafer market compared to multi-crystalline polysilicon ØMono-crystalline polysilicon can only be manufactured using the highest grade Czchoalski (Cz) crucibles ØCz crucibles require the highest purity sand compared to other crucible types ØHPQM is targeting sales to major solar PV/semiconductor industry players (or their preferred Cz crucible suppliers) ØDownstream Pv and Semiconductor growth is enormous with US$ Billions invested and more scheduled ØThe Downstream markets depend on reliable and diverse supply of HPQ Sand. High purity sand availability is a critical factor to solar and semiconductor industry growth.

30

31

Use of Funds A$ Totals Month 1 Month 2 Month 3

Lease and Extension Costs

65,000

15,000 50,000

80,000

10,000 35,000 35,000 HP5/HP7 Testing & Samples

40,000

15,000 15,000 10,000

Total Capex 185,000 40,000 100,000 45,000

30,000

15,000 Key Staff /Consultants/Contractors

135,000

45,000 45,000 45,000 Overheads - Rent/Travel/Sundries

60,000

20,000 20,000 20,000

Total Opex 225,000 65,000 80,000 80,000

Fund raising costs/IPO prep

122,000

47,000 25,000 50,000

Total for Program 532,000

152,000 205,000 175,000

Fund raising and IPO prep costs of A$122k includes A$22k costs related to this equity issue. Net raise is A$510k for the work program as outlined.

32

Indicative returns based on Management view of entry equity valuation at each subsequent funding round Initial A$1m founder investment is notional based on estimated opportunity cost and the value of work done by founders to develop the opportunity to current status. DCF valuation is based on milestone achievement and related reduction of risk discount (included to highlight the potential net present valuation of future cashflows at each round)

Valuation A$millions This Round Round 1a Round 1b Round 2/IPO This Round 0.500 $ Later Rounds 2.5 $ 5.0 $ 30.0 $ Cumulative Total Investments 1.0 $ 1.500 $ 4.0 $ 9.0 $ 39.0 $

Implied Equity Entry Values

Implied Val at Equity Entry (Seed Inv) 5.0 $ Implied Val at Equity Entry (R1a) 12.50 $ Implied Val at Equity Entry (R1b Inv) 50.0 $ Implied Val at Equity Entry (R2 Inv) 300.0 $ Risked DCF Valuation (A$m) 12 $ 41 $ 54 $ 474 $ 881 $ See through investment multiples This Round Round 1a Round 1b Round 2/IPO This Round 1.0x 2.0x 7.2x 38.9x R1a Investor 1.0x 2.2x 19.4x R1b Investor 1.0x 5.4x

33

ESIC (Early Stage Innovation Company) From 1 July 2016, if an investor acquires newly issued shares in a qualifying ESIC, they may be eligible for the following tax incentives:

affiliates combined in each income year; and

continuously held for at least 12 months and less than ten years may be disregarded. Capital losses

investment in qualifying ESICs in an income year is more than $50,000.

shares are issued to the investor. A company will qualify as an ESIC if it meets both the early stage test and either the 100-point innovation test or principles-based innovation test. HPQM considers that it meets the requirements of these Company tests, so Investors participating in this issue may qualify for advantageous tax treatment. NB Investors should undertake their own investigations in relation to qualification for ESIC incentives

34

Battery storage and solar PV demand growth are correlated to growth in renewable energy targets

need to halt global warming and in setting international climate change targets

energy mix and that trend is likely irreversible

be rewarded

Lithium and High Purity Sand demand is correlated to battery and solar PV growth respectively

Lithium production High Purity Sand production

35

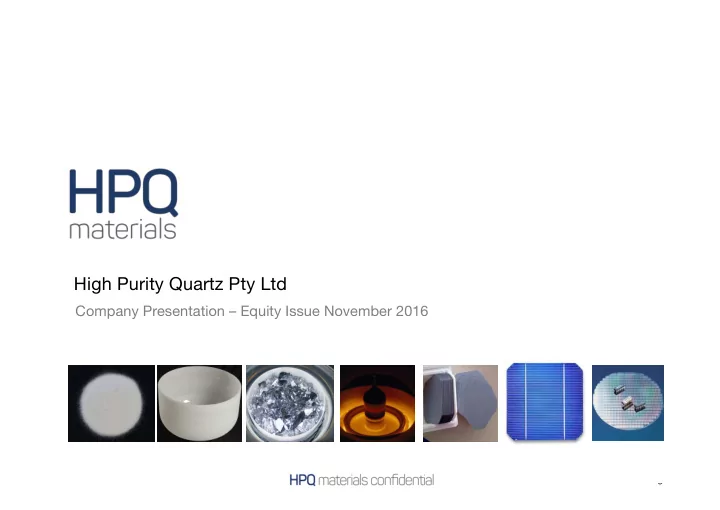

Solar and semi conductor grade crucibles HP7 and HP9 grade HP5 Powder HP5/HP7/HP9 Sand Ex-Townsville Quartz 7mm chip Mono-crystalline solar cell Semi-conductor Camera lenses HP5 powder

36

Stuart Jones (Chief Executive Officer) +61 477 847 346 stuart@hpquartz.com Jason May (Chief Technical Officer) +61 425 798 888 jason@hpquartz.com Website www.hpquartz.com