SLIDE 1

Energy Ventures Analysis 1901 N. Moore St. Arlington, VA 22209 - - PowerPoint PPT Presentation

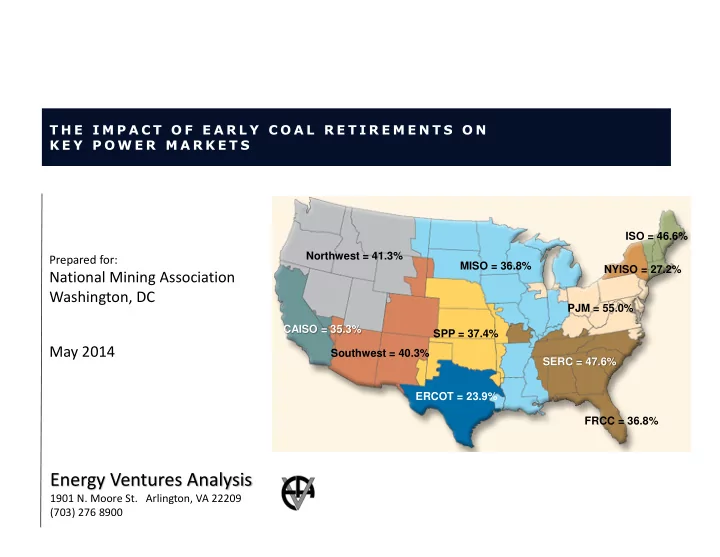

T H E I M P A C T O F E A R L Y C O A L R E T I R E M E N T S O N K E Y P O W E R M A R K E T S ISO = 46.6% Northwest = 41.3% Prepared for: MISO = 36.8% NYISO = 27.2% National Mining Association Washington, DC PJM = 55.0% CAISO =

–

–

–

Region Demand Diff.

Base Capability Base Reserve Post Retire Reserve Retiring Coal Capacity

In

The table to right illustrates what the

PJM wholesale prices would have been

The detailed power analysis section of this

–

–

–

–

–

–

–

–

965 1,332 757 977 1,138 1,403 1,153 738 1,497 693 1,028 1,249 1,695 1,572 1,242 1,665 1,660 1,577 2,473 1,723

(BCF)

Historical 820 590 545

W/O Coal Retirements With Coal Retirements (14/15) With Coal Retirements (14/15/16)With Coal Retirements (14/15/16) Without Coal Retirements With Coal Retirements (14/15)

Forecasted for March 31, 2014

–

–

–

3,071 2,987 2,788 2,886 3,185 3,068 2,713 3,132 3,172 3,155 3,302 3,194 3,452 3,565 3,390 3,810 3,861 3,804 3,929 3,816

Historical 3,380 2,765 2,645

W/O Coal Retirements With Coal Retirements (14/15) With Coal Retirements (14/15/16)With Coal Retirements (14/15/16) Without Coal Retirements With Coal Retirements (14/15)

Forecasted for 2014 (Cold Winter Plus Hot Summer)

–

–

–

–

–