SLIDE 1

1

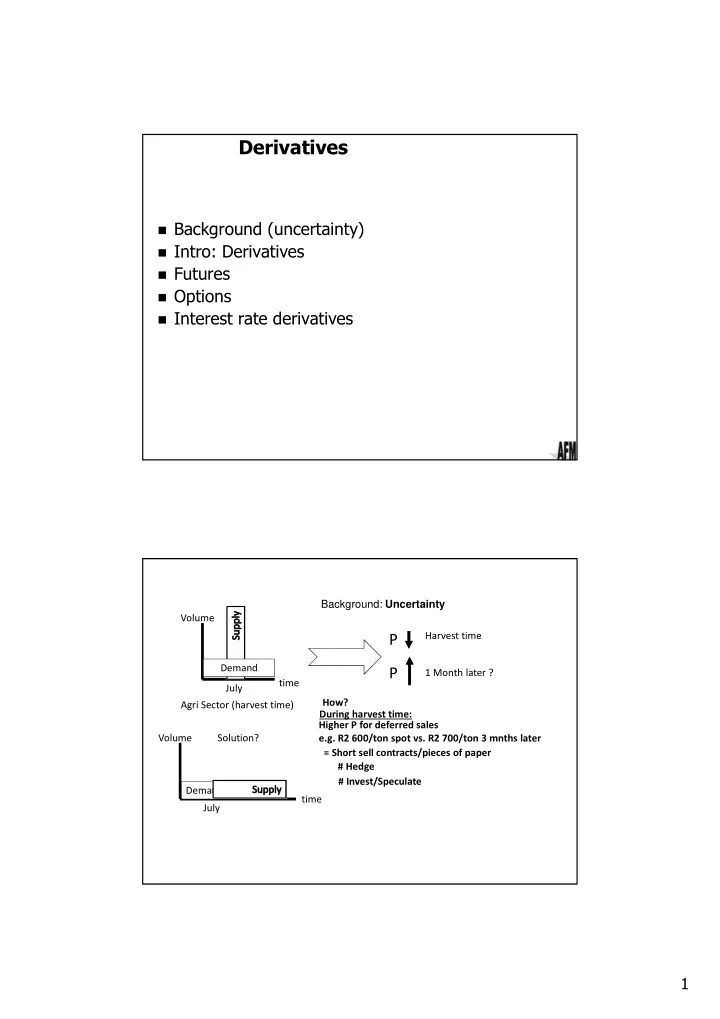

Background (uncertainty) Intro: Derivatives Futures Options Interest rate derivatives

Derivatives

Background: Uncertainty Volume time July Agri Sector (harvest time)

P

Harvest time

P

1 Month later ? Solution? Demand Volume time July Demand During harvest time: How? Higher P for deferred sales = Short sell contracts/pieces of paper # Hedge # Invest/Speculate e.g. R2 600/ton spot vs. R2 700/ton 3 mnths later

SLIDE 2 2

Intro: Derivatives A B C D

You are currently @ A & expect (fear) trend A to B for a specific share price

Would you go long/short at:

You are currently @ B & expect (fear) trend B to C for a specific share price Would you go long/short at:

Repeat the above for expectations/fears about option premiums Repeat the above for expectations/fears about future prices

Defin Long vs. short

Intro Derivatives

Misconceptions Derivatives First seller (“issuer”) = short = bearish (or fear that) Long = bullish (or fear that) Every long pos. has short pos. Derivatives uses – Hedging or Investments

SLIDE 3

3

Intro Derivatives

Today + e.g. 3 months Spot Price Definite trade @ FP (long & short) FP

Future vs. Option

St.P Possible trade @ St.P (long decides) OTC = Full Premium (long pays) No cost, but IM (possible VM)

Open positions on maturity => possible/defin trade Close out prior to maturity => No trades on maturity

Listed = Partial Premium via IM

Pricing General

FP Spot P CoC

Fwd contract with a few “wrinkles”

Pricing Ex. 4

Futures

Extra question: If the actual FP was R11 000/ fine ounce at the beginning, was it over or under valued relative to FFV?

SLIDE 4 4

Futures

SSF Example

At 10:00 on 1 Feb, Mr Seb went long on 3 BHP futures @ R265/share (spot price = R260/share). At the end of the day the BHP future MTM was R264.50/share . The IM was R2000/contract.

- 2. Show his CF on the future on the first day (ignore VM)

- 3. Say the mkt value of BHP was R278.25 at close out,

calculate his overall futures profit (loss)

- 1. Compare the initial capital outlay - underlying vs. futures

(ignore V.Margin) on 1 Feb

- 4. What was his max potential loss on 1 Feb?

- 5. If he had a short position on 1 Feb, what was his max

potential loss?

- 6. What was his gearing (x times) on 1 Feb?

Futures

Index future (newspaper clipping)

Calculate exposure for 1 long futures Calculate exposure for 1 short futures No delivery = No trade on maturity

SLIDE 5

5

Writer Holder Option Premium Long Short Option

Parties Health warning long party

Wasted asset (see pricing)

Calls vs. Puts Call example (notes) + sketch Terminology neutral e.g. ITM, OTM, ATM, etc

Option

Example 6 Additional questions Capital outlay – long 100 Billiton vs. long 100 SBN Max loss on the above?

SLIDE 6

6

Exposure (underlying) = int. rates

Interest rate derivatives

To benefit/hedge @ rising int. rates: Buy FRAs Buy IRS