SLIDE 1

BMS HND - FA - Dhanushka Abeysekara 1

Chapter 14

Concepts

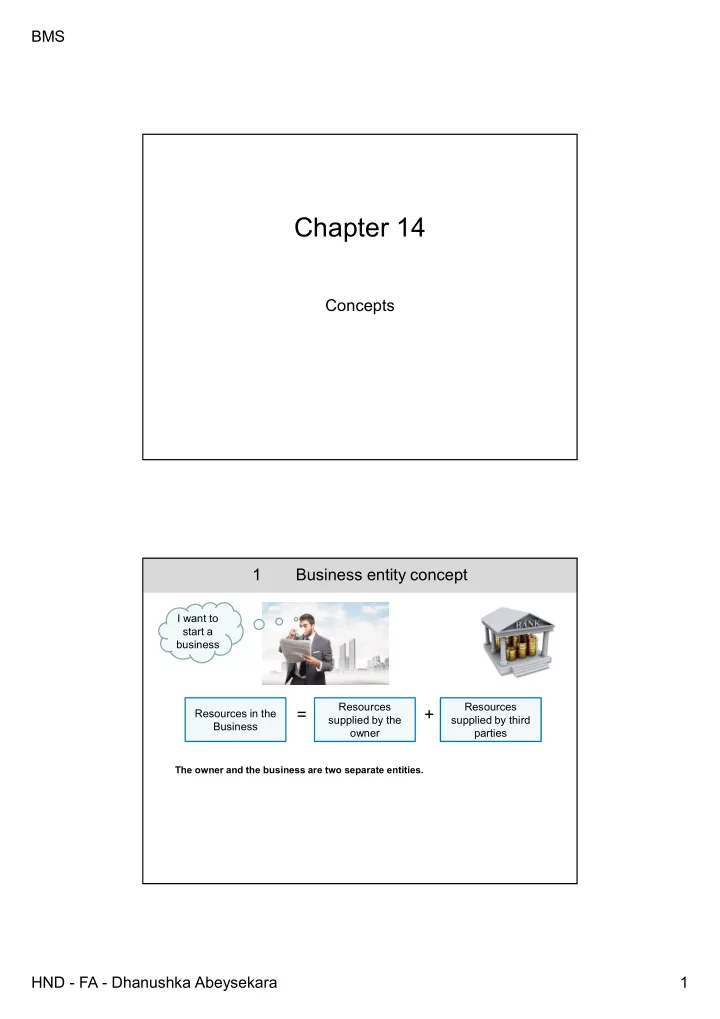

I want to start a business Resources in the Business Resources supplied by the

- wner

Resources supplied by third parties

= +

Assets = Capital + Liabilities The owner and the business are two separate entities.