SLIDE 7 7

Analysis: Allocation – Europe versus the U.S.

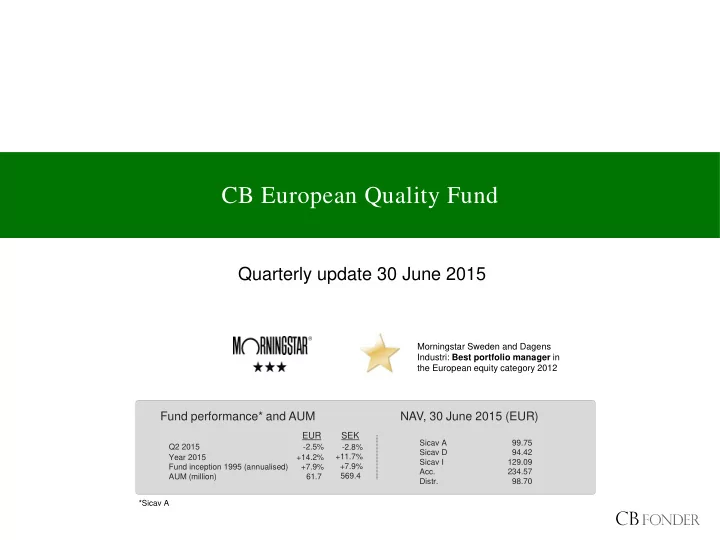

CB European Quality Fund

MSCI Europe relative to MSCI USA. Periods of out-/underperformance MSCI Europe relative to MSCI USA, in USD

- Europe has performed better than the

U.S., with data going back to 1969.

- Europe has four pronounced periods of

underperformance against the U.S., all

which have bottomed when the accumulated underperformance reached ~40% - the same level that was reached at year-end 2014.

argue that a new period

- f

- utperformance has started for Europe –

and so far you have missed almost nothing (+2% since the trough at year- end 2014/2015).

Source: MSCI, CB Fonder

Since 1969 there have been three periods of outperformance for Europe relative to the U.S. – now we are seeing the start of a fourth?

- The three periods of outperformance for

Europe relative to the U.S. lasted between 24 and 101 months and resulted in an accumulated relative

- utperformance of between 75 and 102

percent (see graph).

- The current period of outperformance

(red line) mostly reminds of the period starting in 1999 (dark blue line). It could therefore be argued that there is no rush to buy Europe. On the other hand, with the same logic one could say that there is only upside risk for Europe…

Number of months Outperformance, Europe relative USA

From To

1 975- 02- 28 1 976- 1 0- 29

8% 30%

1 976- 1 0- 29 1 978- 1 0- 31 76%

84% 1 978- 1 0- 31 1 985- 02- 28 34% 1 32%

1 985- 02- 28 1 990- 1 0- 31 283% 90% 1 02% 1 990- 1 0- 31 1 999- 06- 30 224% 451 %

% 1 999- 06- 30 2007- 1 1

1 02% 1 5% 75% 2007- 1 1

201 4- 1 2- 31

56%

% 201 4- 1 2- 31 201 5- 06- 30 4% 1 % 2%

MSCI Europe MSCI USA Relative return Time period Absolute return, USD