SLIDE 1

Threshold Models

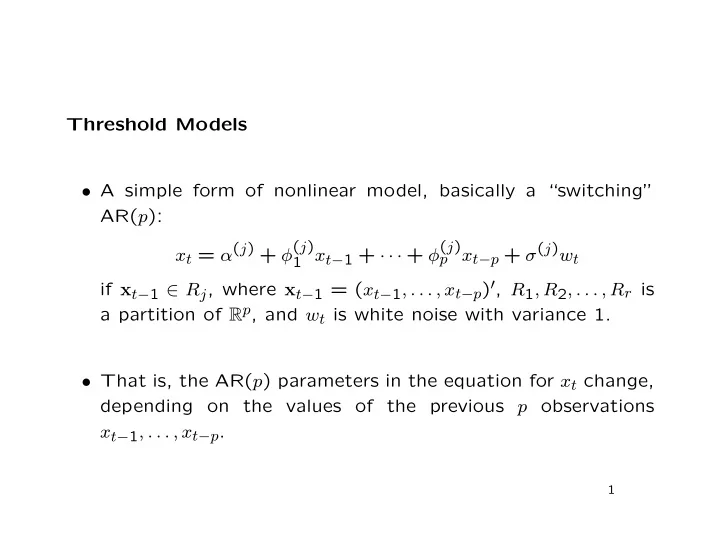

- A simple form of nonlinear model, basically a “switching”

AR(p): xt = α(j) + φ(j)

1 xt−1 + · · · + φ(j) p xt−p + σ(j)wt

if xt−1 ∈ Rj, where xt−1 = (xt−1, . . . , xt−p)′, R1, R2, . . . , Rr is a partition of Rp, and wt is white noise with variance 1.

- That is, the AR(p) parameters in the equation for xt change,