SLIDE 1

1

Applications Division

July 19, 2018

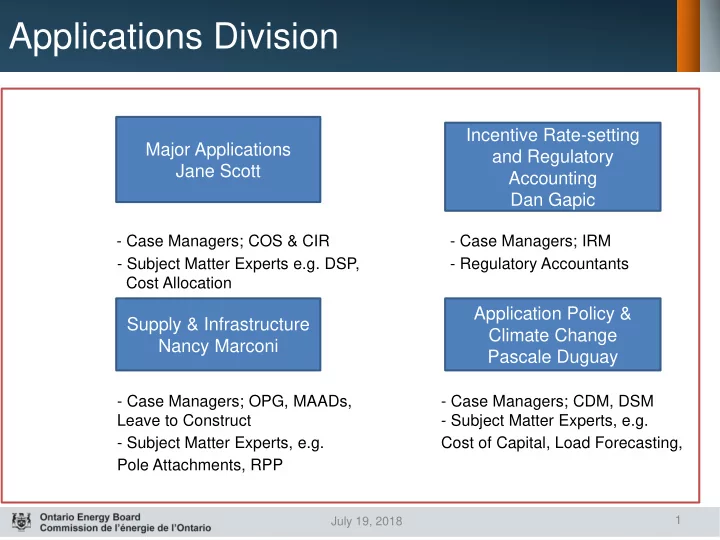

- Case Managers; COS & CIR

- Case Managers; IRM

- Subject Matter Experts e.g. DSP,

- Regulatory Accountants

Cost Allocation

- Case Managers; OPG, MAADs,

- Case Managers; CDM, DSM

Leave to Construct

- Subject Matter Experts, e.g.

- Subject Matter Experts, e.g.

Cost of Capital, Load Forecasting, Pole Attachments, RPP

Major Applications Jane Scott Incentive Rate-setting and Regulatory Accounting Dan Gapic Supply & Infrastructure Nancy Marconi Application Policy & Climate Change Pascale Duguay