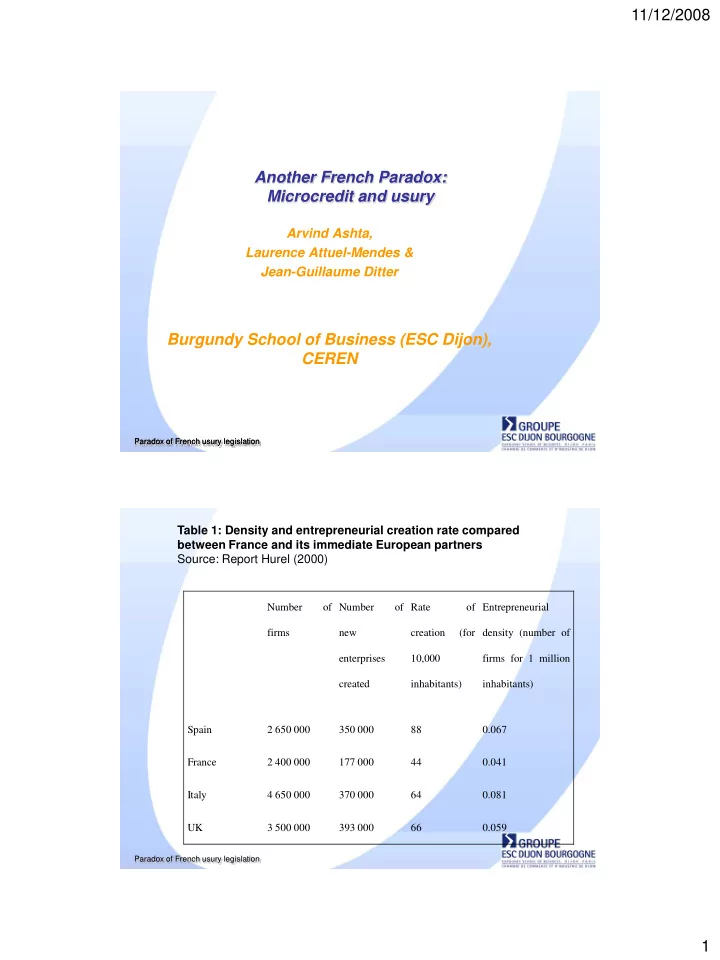

SLIDE 4 11/12/2008 4

Paradox of French usury legislation

Loans to enterprises

0,00 2,00 4,00 6,00 8,00 10,00 12,00 14,00 16,00 2002 2003 2004 2005 2006 2007 Time (year centred on first quarter) Interest rates (%) Suppliers credit and Hire purchase (av erage rate) Suppliers credit and Hire purchase (usury ceiling) Variable rate Term loans (> 2yrs) (av erage rate) Variable rate Term loans (> 2yrs) (usury ceiling) Fixed rate term loans (> 2 yrs) (av erage rate) Fixed rate term loans (> 2 yrs) (usury ceiling) Ov erdraft (av erage rate) Ov erdraft (usury ceiling) Other short term loans (< 2 yrs) (av erage rate) Other short term loans (< 2 usury ceilings av erage rates

Housing loans to individuals

0,00 1,00 2,00 3,00 4,00 5,00 6,00 7,00 8,00 9,00 2002 2003 2004 2005 2006 2007 Time (year centred on first quarter) Interest rates (%) Fixed rate loans (average rate) Fixed rate loans (usury ceiling) Variable rate loans (average rate) Variable rate loans (usury ceiling) Bridge loans (average rate) Bridge loans (usury ceiling) usury ceilings average rates

Other loans to individuals

0,00 5,00 10,00 15,00 20,00 25,00 2002 2003 2004 2005 2006 2007 Time (year centred on first quarter) Interest rates (%) Small loans of less than 1524 Euros (average rate) Small loans of less than 1524 Euros (usury ceiling) Overdraft, hire purchase and term loans of more than 1524 Euros (average rate) Overdraft, dererred credit and term loans of more than 1524 Euros (usury ceiling) Personal loans of more than 1524 euros (average rate) Personal loans of more than 1524 euros (usury ceiling) usury ceilings average rates

Source: Bank of France data

Figure 2: Interest Rates and Usury Celings in France (2002-2007) Interest rates don't seem to have gone up exceptionally. If they went up, this may be global interest rate rise

Paradox of French usury legislation

Figure 3: Interest spreads and maximum usury spreads in France (2002-2007)

Housing loans to individuals 0,00 1,00 2,00 3,00 4,00 5,00 6,00 2002 2003 2004 2005 2006 2007 Time (year centred on first quarter) Interest rates (%)

Fixed rate loans (average rate) Fixed rate loans (usury ceiling) Variable rate loans (average rate) Variable rate loans (usury ceiling) Bridge loans (average rate) Bridge loans (usury ceiling) usury ceilings average rates

Other loans to individuals 0,00 5,00 10,00 15,00 20,00 25,00 2002 2003 2004 2005 2006 2007 Time (year centred on first quarter) Interest rates (%)

Small loans of less than 1524 Euros (average rate) Small loans of less than 1524 Euros (usury ceiling) Overdraft, hire purchase and term loans of more than 1524 Euros (average rate) Overdraft, dererred credit and term loans of more than 1524 Euros (usury ceiling) Personal loans of more than 1524 euros (average rate) Personal loans of more than 1524 euros (usury ceiling) usury ceilings average rates

Loans to entreprises 0,00 2,00 4,00 6,00 8,00 10,00 12,00 2002 2003 2004 2005 2006 2007 Time (year centred on first quarter) Interest rates (%)

Suppliers credit and Hire purchase (average rate) Suppliers credit and Hire purchase (usury ceiling) Variable rate Term loans (> 2yrs) (average rate) Variable rate Term loans (> 2yrs) (usury ceiling) Fixed rate term loans (> 2 yrs) (average rate) Fixed rate term loans (> 2 yrs) (usury ceiling) Overdraft (average rate) Overdraft (usury ceiling) Other short term loans (< 2 yrs) (average rate) Other short term loans (< 2 yrs) (usury ceiling) usury ceilings average rates

Derived from bank of France data

Spreads seem to be reducing !!!