SLIDE 1

ANNUAL GENERAL MEETING 2018

Sydney 30 October 2018

2

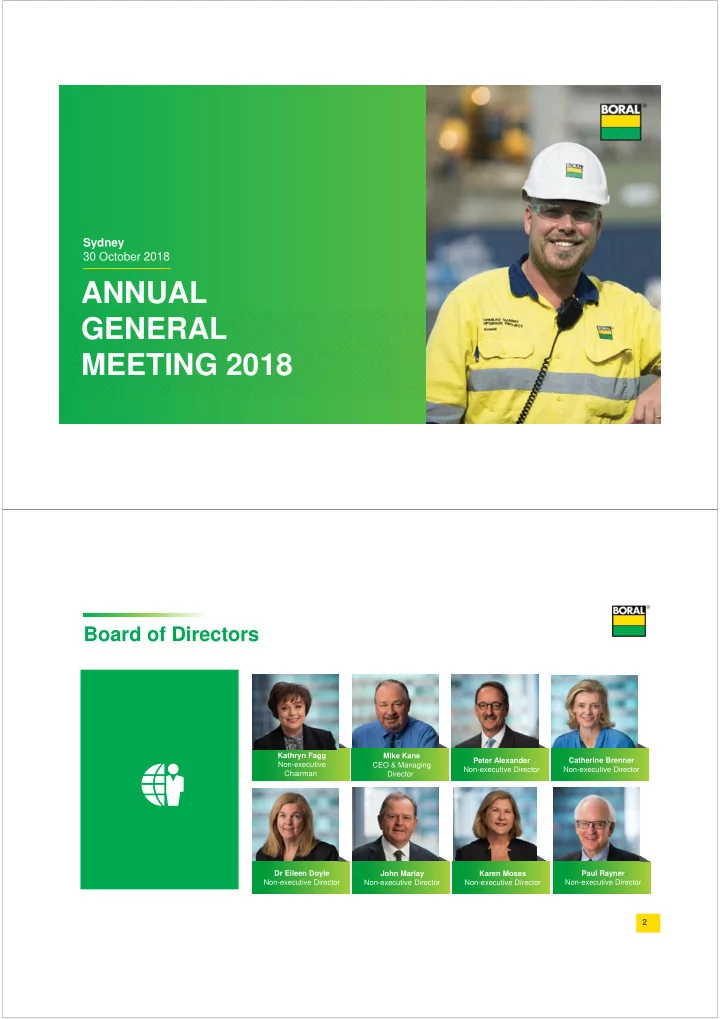

Board of Directors

- Karen Moses

- Non-executive Director

- Mike Kane

- CEO & Managing

Director

- John Marlay

- Non-executive Director

- Dr Eileen Doyle

- Non-executive Director

- Kathryn Fagg

- Non-executive

Chairman

- Peter Alexander

- Non-executive Director

- Catherine Brenner

- Non-executive Director

- Paul Rayner

- Non-executive Director