SLIDE 1

1

1

2006 Half Year Results Presentation

6 months to 30 June 2006

10 August 2006

2

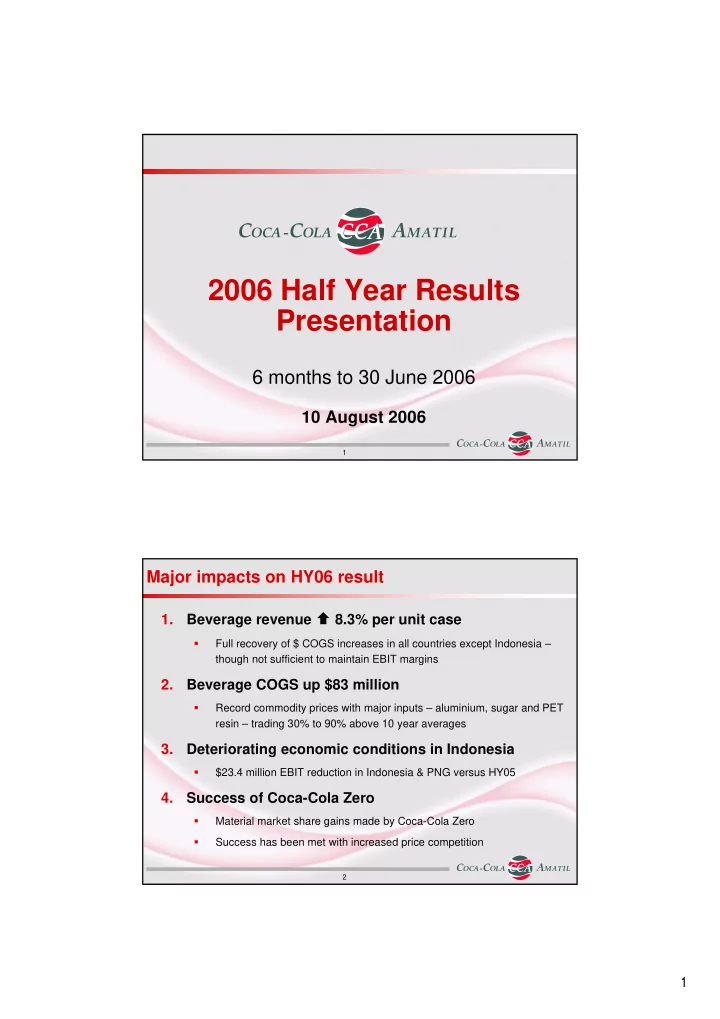

Major impacts on HY06 result

1. Beverage revenue 8.3% per unit case

- Full recovery of $ COGS increases in all countries except Indonesia –

though not sufficient to maintain EBIT margins

2. Beverage COGS up $83 million

- Record commodity prices with major inputs – aluminium, sugar and PET

resin – trading 30% to 90% above 10 year averages

3. Deteriorating economic conditions in Indonesia

- $23.4 million EBIT reduction in Indonesia & PNG versus HY05

4. Success of Coca-Cola Zero

- Material market share gains made by Coca-Cola Zero

- Success has been met with increased price competition