SLIDE 1

10/11/2013 1

Income Security & Aging

Christopher M. Kelly, Ph.D. UNO Department of Gerontology October 16, 2013

Financial Status of Older Adults

- Since Great Depression, financial status of

- lder Americans has improved

- Median incomes for 65+ has risen; poverty

rates for 65+ have dropped

- Financial status within 65+ population

varies significantly

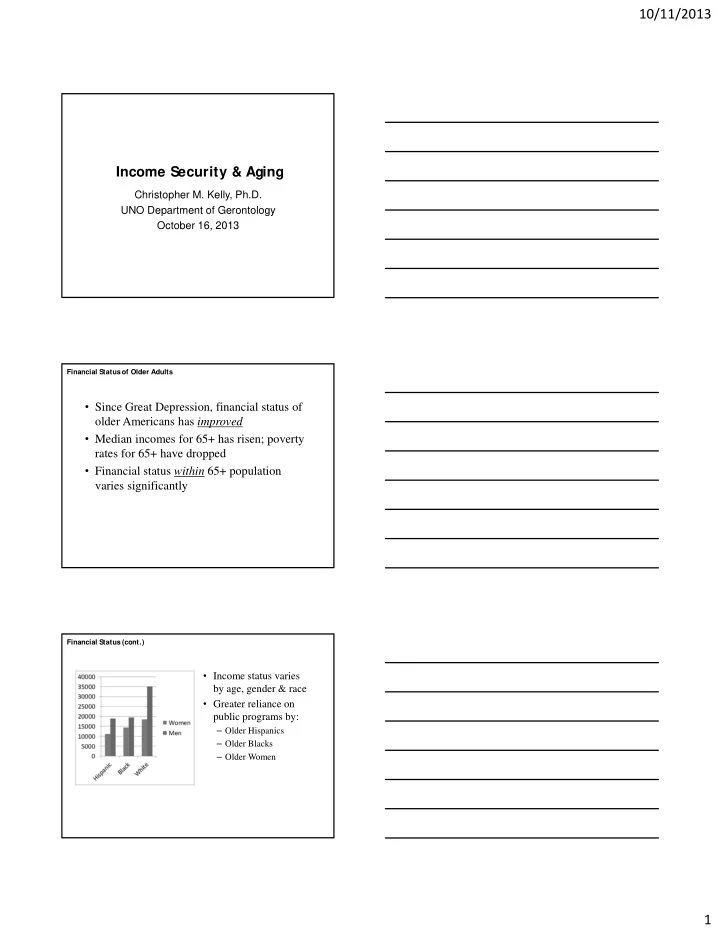

Financial Status (cont.)

- Income status varies

by age, gender & race

- Greater reliance on