SLIDE 1

Greg Blonder April 2011

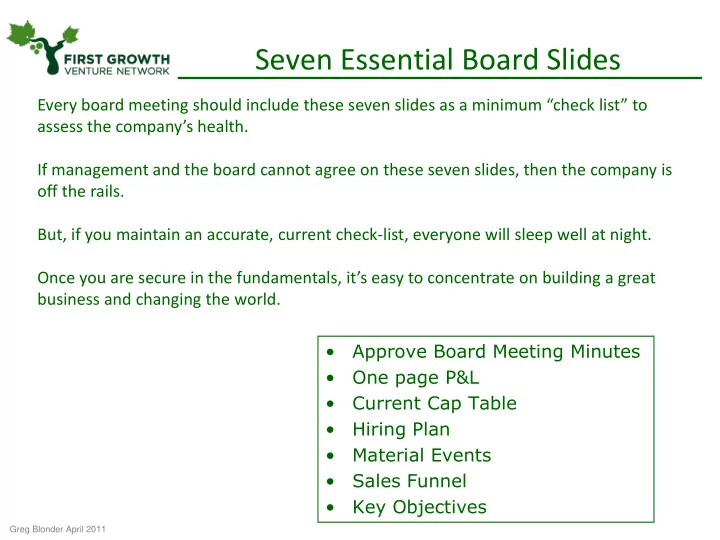

Seven Essential Board Slides

- Approve Board Meeting Minutes

- One page P&L

- Current Cap Table

- Hiring Plan

- Material Events

- Sales Funnel

- Key Objectives

Every board meeting should include these seven slides as a minimum “check list” to assess the company’s health. If management and the board cannot agree on these seven slides, then the company is

- ff the rails.

But, if you maintain an accurate, current check-list, everyone will sleep well at night. Once you are secure in the fundamentals, it’s easy to concentrate on building a great business and changing the world.