SLIDE 1

Reverberating Mergers in the Food Chain Post-2014 Flour Post-2015 - - PowerPoint PPT Presentation

Reverberating Mergers in the Food Chain Post-2014 Flour Post-2015 Cereal Seed CR-2 FTC Wave of Mergers CR-4 Merger CR-4 Blocked Supermark 77% Sysco- et mergers 85% 64% USFoods exceeds 66% merger to the late monopoly 1990s Corn

77% 66% Corn Soybean

Seed CR-2

64%

Post-2014 Flour Mergers CR-4

85%

Post-2015 Cereal Merger CR-4

FTC Blocked Sysco- USFoods merger to monopoly Wave of Supermark et mergers exceeds the late 1990s

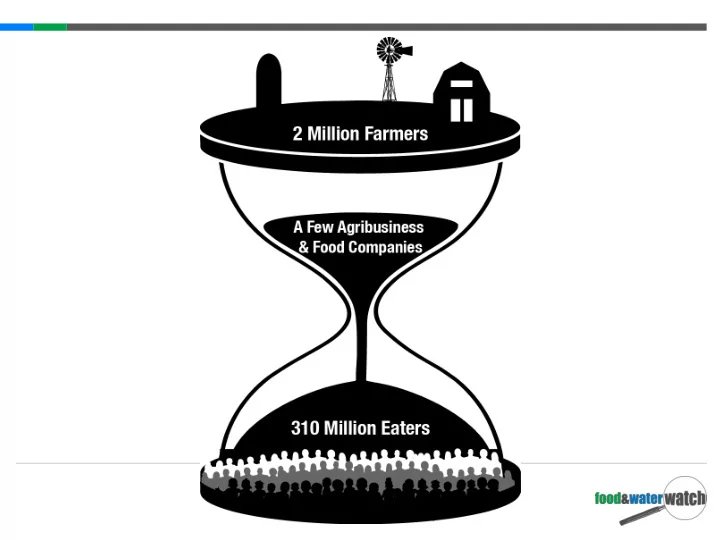

Seeds Farms Flour Mill Cereal Factory Distribution Supermarket Home

Source: USDA GIPSA

35.8% 36.6% 43.8% 54.3% 55.0% 65.0% 64.0%

1982 1987 1992 1997 2002 2007 2011

23.8 23.5 26.8 27.5 41.2 47.3 $5.8 $4.8 $3.9 $4.1 $3.7 $5.1 1982 1987 1992 1997 2002 2007 Hogs Sold (millions) Value of Hogs Sold (billions 2010 dollars)

Source: USDA; Food & Water Watch The Cost of Food Monopolies

Source: USDA; Food & Water Watch The Cost of Food Monopolies

49,000 38,600 34,000 18,400 11,300 8,800 470 584 747 1,454 3,852 5,068

1982 1987 1992 1997 2002 2007 Hog Farms Hogs sold per farm

from Maryland’s Eastern Shore: nearly $1 billion in 2007

$280 for every 1,000 birds

annually after paying $70,000 to service their debt

$848 $83 $25

Poultry/Egg "Sales" Total Farmer Broiler Receipts Farmer Net Earnings

Maryland E. Shore Poultry Value

(2007 in millions)

Production Share of Selected Crops & Livestock

2.0% 50.3% 61.0% 47.7% 59.5% 84.7% 38.4% 3.5% 9.0% 2.0% 2.5% 17.5% 6.4% 32.0% 18.0% 2.2%

Beef Cattle Hogs Dairy Broilers Vegetables Corn Wheat Orchards

1940 2007

Maryland’s Eastern Shore went from diversified operations

to a few farms producing mostly broilers and feed

Source: USDA

Dry Mac & Cheese (79.9%)

Hispanic Food (1.7%)

Processed Cheese (48.3%)

Peanut Butter (2.4%)

Lunch Meat (34.8%)

Refrig./Fzn. Cakes & Pies (3.7%)

Mayonnaise (33.9%)

Pickles, Olives, Relish (7.5%) Meat Sauces (24.0%) Mustard (12.6%) Fruit Drinks (20.7%)

Shelf- Stable Dips (8.1%)

Salad Dressing (20.5%) Bacon (20.3%) Cottage Cheese (20.2%) Sour Cream (18.3%) Nuts (17.9%) Natural Cheese (17.3%) Hot Dogs (19.8%) Breakfast Meat (14.8%) Meat Substitute (14.7%) Coffee (14.0%)

Source: Food & Water Watch, Grocery Goliaths

Dry Mac & Cheese (78.0%)

Hispani c Food (4.5%)

Processed Cheese (54.3%) Lunch Meat (34.8%)

Mayonnaise (33.1%)

Pickles, Olives, Relish (6.7%) Meat Sauces (77.9%) Mustard (10.7%) Fruit Drinks (13.7%) Salad Dressing (17.6%) Bacon (18.7%)

Cottage Cheese (23.2%) Nuts (26.1%)

Natural Cheese (17.9%) Meat Substitute (12.9%) Coffee (13.5%)

Cooking Sauce (9.9%)

Ketchup (63.2%)

Pasta Sauce (10.6%) Peanut Butter (2.1%) Spices (1.6%)

Hot Dogs (20.2%)

Frozen Appetizers (20.1%) Frz. Handheld Entrée (2.6%) Frozen Snacks (9.4%)

Source: Mintel

17.0% 20.8% 28.8% 34.0% 30.9% 34.0% 50.7% 53.1% 1994 1997 1998 1999 2002 2004 2009 2015

Source: Univ. Minnesota; ERS USDA; USDA/DoJ; Census Bureau; Supermarket News; Food & Water Watch analysis. * post Abertsons-Safeway merger.

Market Share of Four Largest Grocery Retailers

2004

Source: Food & Water Watch analysis of MetroMarket data.

2011

Source: Food & Water Watch analysis of MetroMarket data.

87.9% 80.8% 82.7% 79.9% 75.7% 76.7% 75.8% 68.7% 64.8% 63.8% 60.3% 92.0% 87.0% 86.7% 85.0% 78.9% 78.7% 74.2% 73.2% 68.1% 67.5% 60.6% Soda* Chocolate Performance Bars Breakfast Cereal Potato Chips Ketchup**

Coffee Lunch Meat

2010-2011 2014-15

Source: F&WW Grocery Goliaths and preliminary update; * only 3 major firms, ** only 2 firms in 2014/5

Source: FWW Analysis

Source: FWW Analysis

Source: FWW Analysis

0% 5% 10% 15% 20% 25% 30% 35% 40%

50 100 150 200 250

1984 1989 1994 1999 2004 2009 Farmer Share Retail index (1982-84 = 100)

Retail Cost Farm Share

Source: USDA National Agricultural Statistical Service; market basket of foods that are only primarily originated on farms like fruits, vegetables and milk.

$11.70 $21.90 $11.80 50 100 150 200 250

Fresh Whole Milk CPI Cheese CPI Farmgate Milk ($/100 gal.)

Source: USDA; Census Bureau.

3.8% 3.2% 2.9% 1.5% 1.2% 1.1% 1.0% 0.8% 0.8% 0.4%

Eggs Ground beef Potatoes Pasta Bread Peanut butter Apples Cheddar cheese Broccoli Hourly wages Milk Bologna Processed cheese

Source: Food & Water Watch analysis of Bureau of Labor Statistics data.

2000-2012

$17.0 $11.0 $9.9 $5.7

Commodities Food Manufacturers Seed, Agrochemical, Veterinary and Biotechnology Meatpackers, Poultry

(millions)

Source: Food & Water Watch Cultivating Influence