Office of Inspector General

NSF Grants Conference June 1-2, 2015

William J. Kilgallin Senior Advisor, Investigations Office of Inspector General National Science Foundation

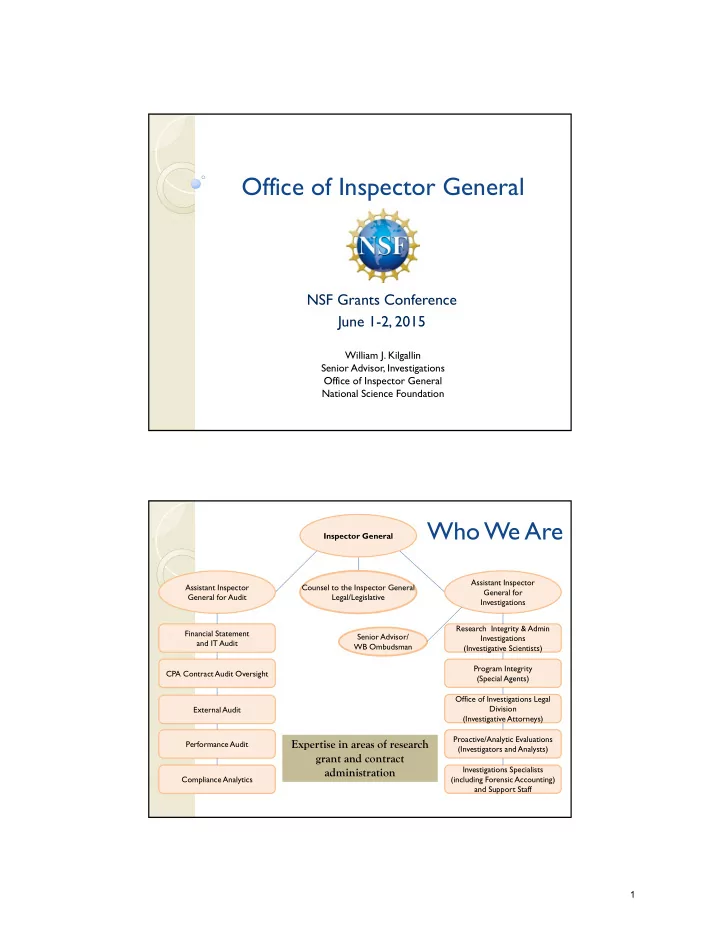

Who We Are

Assistant Inspector General for Investigations Assistant Inspector General for Audit Inspector General Counsel to the Inspector General Legal/Legislative Research Integrity & Admin Investigations (Investigative Scientists) Program Integrity (Special Agents) Office of Investigations Legal Division (Investigative Attorneys) Proactive/Analytic Evaluations (Investigators and Analysts) Financial Statement and IT Audit CPA Contract Audit Oversight External Audit Performance Audit

Expertise in areas of research grant and contract administration

Senior Advisor/ WB Ombudsman Investigations Specialists (including Forensic Accounting) and Support Staff Compliance Analytics

1