SLIDE 1

1

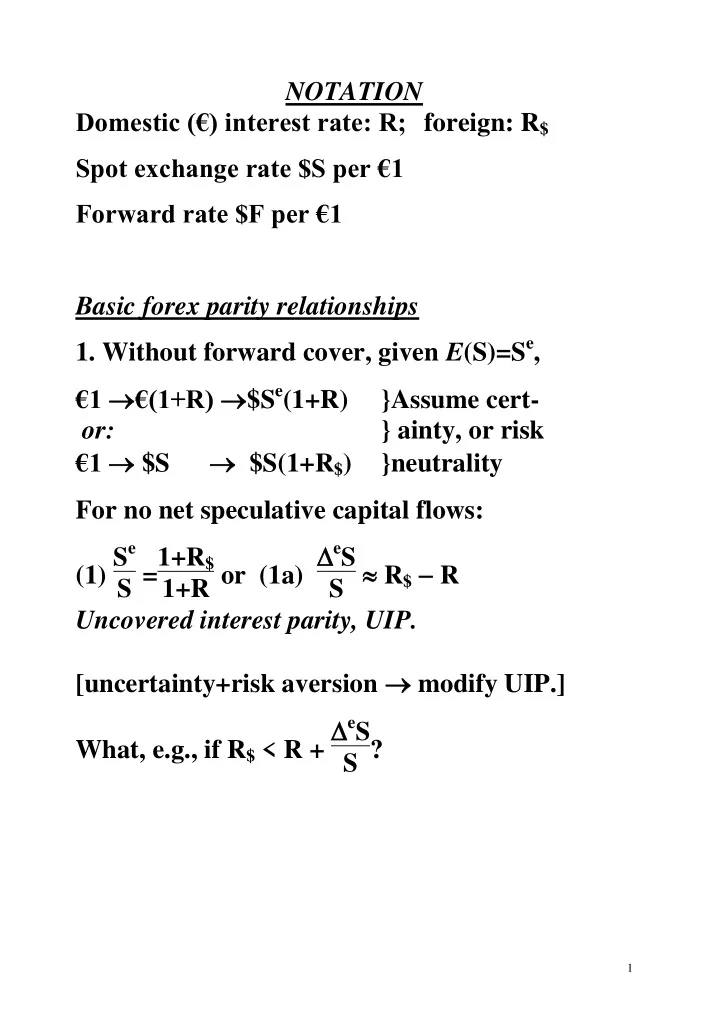

NOTATION Domestic (€) interest rate: R; foreign: R$ Spot exchange rate $S per €1 Forward rate $F per €1 Basic forex parity relationships

- 1. Without forward cover, given E(S)=Se,

€1 €(1+R) $Se(1+R) }Assume cert-

- r: