1

News Release

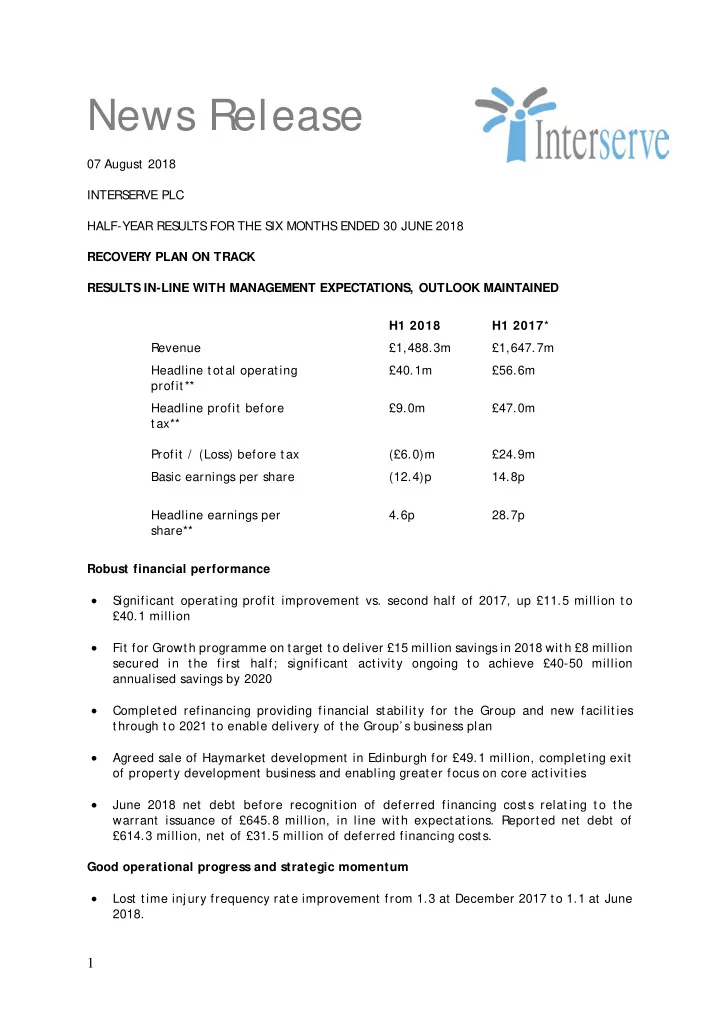

07 August 2018 INTERS ERVE PLC HALF-YEAR RES ULTS FOR THE S IX MONTHS ENDED 30 JUNE 2018 RECOVERY PLAN ON TRACK RESULTS IN-LINE WITH MANAGEMENT EXPECTATIONS, OUTLOOK MAINTAINED H1 2018 H1 2017* Revenue £1,488.3m £1,647.7m Headline t ot al operat ing profit ** £40.1m £56.6m Headline profit before t ax** Profit / (Loss) before t ax £9.0m (£6.0)m £47.0m £24.9m Basic earnings per share (12.4)p 14.8p Headline earnings per share** 4.6p 28.7p Robust financial performance

- S

ignificant operat ing profit improvement vs. second half of 2017, up £11.5 million t o £40.1 million

- Fit for Growt h programme on t arget t o deliver £15 million savings in 2018 wit h £8 million

secured in t he first half; significant act ivit y ongoing t o achieve £40-50 million annualised savings by 2020

- Complet ed refinancing providing financial st abilit y for t he Group and new facilit ies

t hrough t o 2021 t o enable delivery of t he Group’ s business plan

- Agreed sale of Haymarket development in Edinburgh for £49.1 million, complet ing exit

- f propert y development business and enabling great er focus on core act ivit ies

- June 2018 net debt before recognit ion of deferred financing cost s relat ing t o t he

warrant issuance of £645.8 million, in line wit h expect at ions. Report ed net debt of £614.3 million, net of £31.5 million of deferred financing cost s. Good operational progress and strategic momentum

- Lost t ime inj ury frequency rat e improvement from 1.3 at December 2017 t o 1.1 at June

2018.