Helvetas Vietnam

Regional Workshop on Beef markets and trade in China and Southeast Asia China country profile

Wang Jimin, Zhang Huijie, Dong Xiaoxia, Wang Mingli (Chinese Academy of Agricultural Sciences) Scott Waldron (the University of Queensland)

Macro drivers and priorities

! Rapid economic growth has

! Increased rural incomes – reduced incentives for small-holders to raise cattle ! and urban incomes – increased consumption

! Government priorities

! Concern with food price inflation, food safety and “modernization”

! Agribusiness activity

! (Over) investment in agro-industry (feedlots, modern abattoirs, retail, often integrated)

! Socio-economic importance

! Cattle production is significant but becoming less important in the rural economy ! But beef important in diet for some ethnic minorities

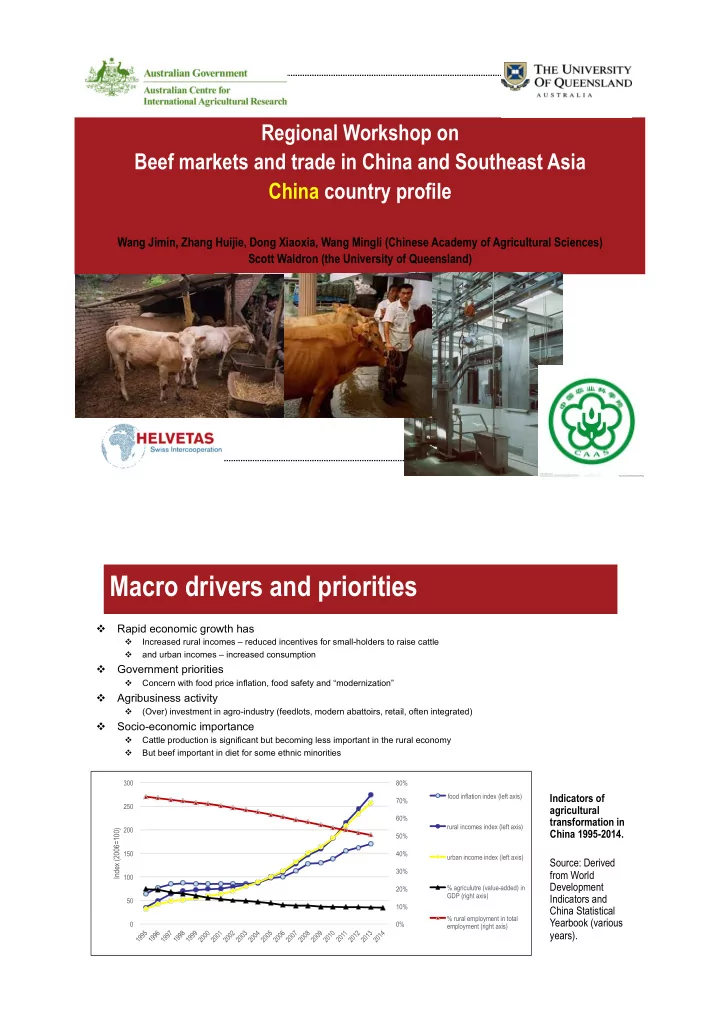

0% 10% 20% 30% 40% 50% 60% 70% 80% 50 100 150 200 250 300

Index (2006=100)

food inflation index (left axis) rural incomes index (left axis) urban income index (left axis) % agriculutre (value-added) in GDP (right axis) % rural employment in total employment (right axis)

Indicators of agricultural transformation in China 1995-2014. Source: Derived from World Development Indicators and China Statistical Yearbook (various years).