SLIDE 1

INVESTOR PRESENTATION

June 2006

2

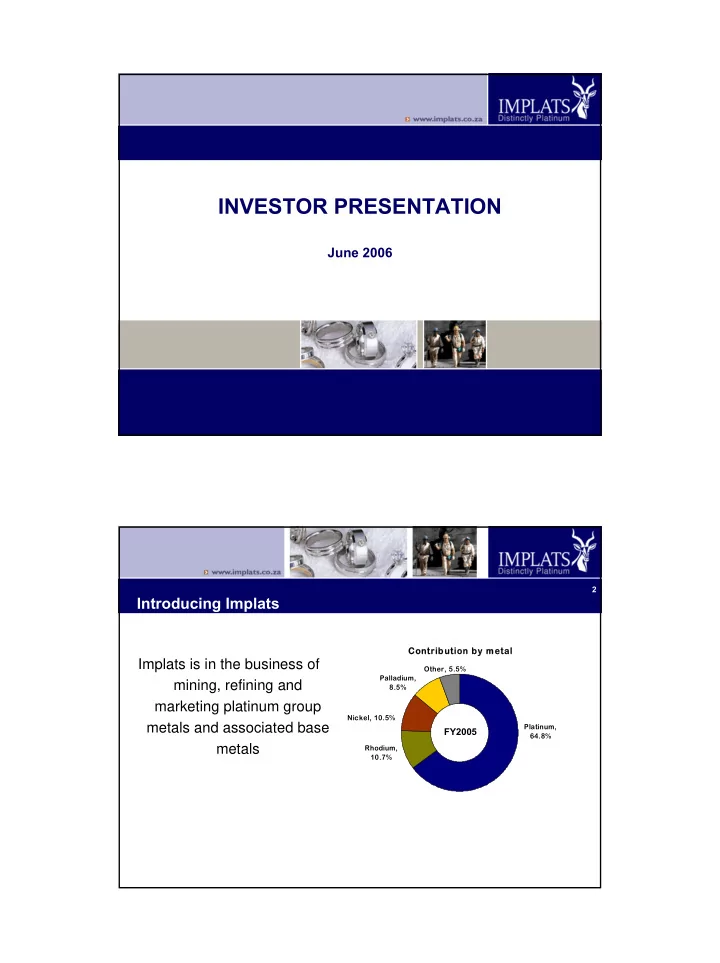

Introducing Implats

Implats is in the business of mining, refining and marketing platinum group metals and associated base metals

Cont

- ntrib

ribution b

- n by m

metal

Platinum, 64.8% Other, 5.5% Palladium, 8.5% Nickel, 10.5% Rhodium, 10.7%

FY2005