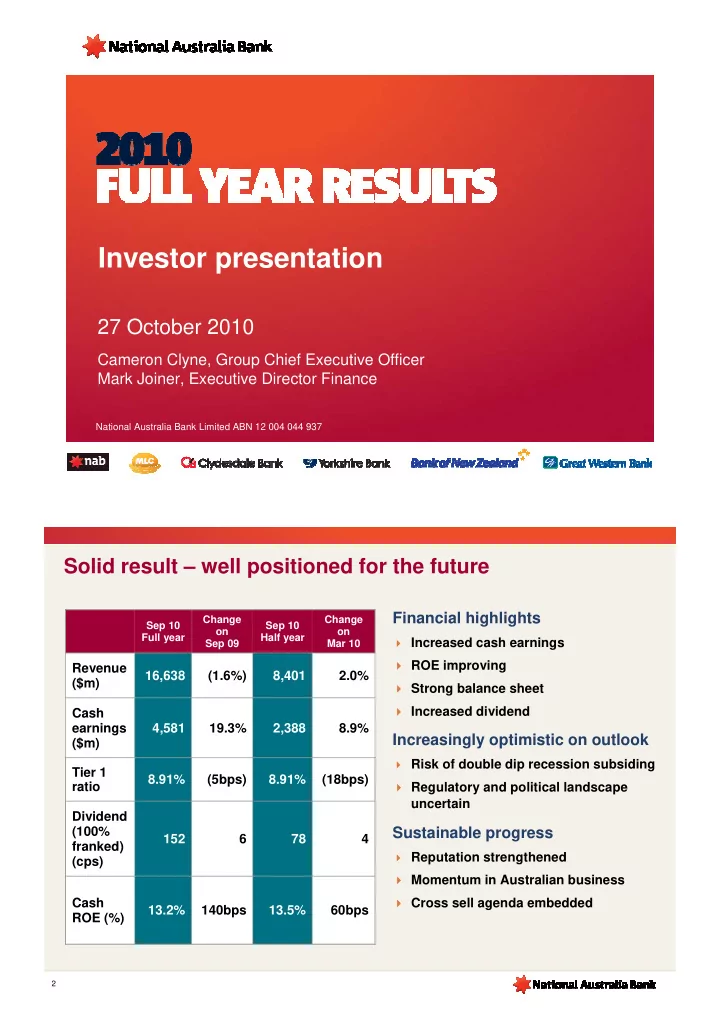

SLIDE 6 11

Key elements of the result (2)

Jaws and banking CTI momentum Operating expenses

2H10 v 1H10 1H10 v 2H09 2H09 v 1H09

1.1%

CTI 2H09

44.5%

CTI 2H10

46.2%

CTI 1H10

45.5%

1.3%

Revenue growth Expense growth

3.6% 2.0%

Other operating income

1,410 1,417 1,263 1,255 760 468 302 213 539 529 748 764 (5) (79) (210) (190)

Mar 09 Sep 09 Mar 10 Sep 10

Fees & Commissions Markets & Treasury MLC Other*

($m) 2,630 2,204 2,123 2,227

SGA portfolio income

($m)

138 127 100 80 (67) (162) (30) (139) (160) (14) (65) (80) (84) 125 (1) (6) (101) Mar 09 Sep 09 Mar 10 Sep 10

SCDO Risk Mitigation MTM Mngmt Overlay for Conduit & derivative trans Markets Counterparty Credit Val Adj Non Franchise Asset Income CDS Hedging MTM volatility

Total income (165) Total income (84) Total income (108) Total income 18

* Includes SGA, Group Treasury and Other

7,580 7,868 7,862 (399) (180) 393 59 254 155

Sep 09 EQS Benefits Investment in Business BAU (net) UK Pension Sep 10 ex FX & Acqn Acquisitions FX Impacts Sep 10 incl FX & Acqn

($m)

CTI – Banking Cost to Income Ratio

12

B&DD charge and asset quality

B&DD charge – half yearly 90+DPD & impaired assets as a % of gross loans and acceptances by product

300 700 1,100 1,500 1,900 2,300

Mar 07 Sep 07 Mar 08 Sep 08 Mar 09 Sep 09 Mar 10 Sep 10

0.00% 0.20% 0.40% 0.60% 0.80% 1.00%

Specific Provision Collective Provision Economic Cycle Adjustment ABS CDOs & Investments held to maturity B&DD Charges as % of GLAs (annualised)

390 400 726 1,763 1,811 2,004 1,230

($m)

1,033 0.0% 0.5% 1.0% 1.5% 2.0% Mar 07 Sep 07 Mar 08 Sep 08 Mar 09 Sep 09 Mar 10 Sep 10

Impaired 90+DPD

Mortgages Impaired Business Impaired Mortgages 90+ DPD Business 90+ DPD Retail Unsecured 90+ DPD

B&DD charge – quarterly

($m)

300 600 900 1,200 Dec 08 Mar 09 Jun 09 Sep 09 Dec 09 Mar 10 Jun 10 Sep 10

824 987 1,064 940 739 491 0.00% 0.25% 0.50% 0.75% 1.00% 1.25% 1.50% 1.75% 2.00% Mar 07 Sep 07 Mar 08 Sep 08 Mar 09 Sep 09 Mar 10 Sep 10

Coverage ratios

Basel II RWAs

510 523

GRCL top up (pre-tax) as % of Credit Risk Weighted Assets (ex Housing) Collective Provisions as % of Credit Risk Weighted Assets (ex Housing) Total Provisions as % Gross Loans and Acceptances