January–September Ratos’s interim report 2019 1

Interim report, January–September 2019

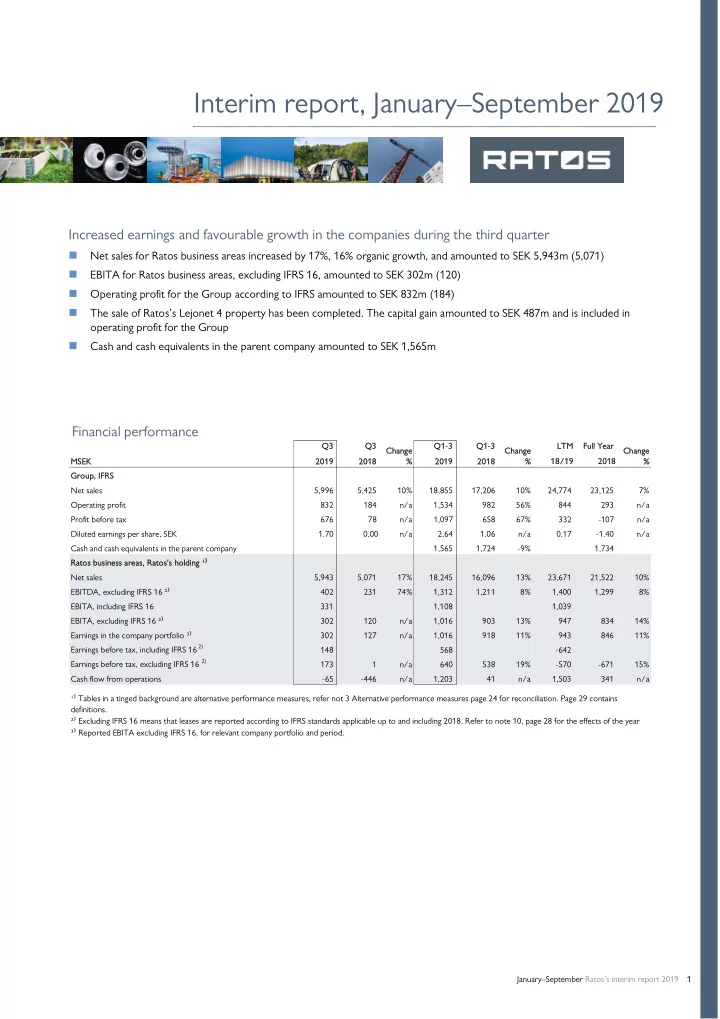

Increased earnings and favourable growth in the companies during the third quarter

Net sales for Ratos business areas increased by 17%, 16% organic growth, and amounted to SEK 5,943m (5,071)

EBITA for Ratos business areas, excluding IFRS 16, amounted to SEK 302m (120)

Operating profit for the Group according to IFRS amounted to SEK 832m (184)

The sale of Ratos’s Lejonet 4 property has been completed. The capital gain amounted to SEK 487m and is included in

- perating profit for the Group

Cash and cash equivalents in the parent company amounted to SEK 1,565m

Financial performance

Q3 Q3 Q3 Q3 Q1 Q1-3 Q1 Q1-3 LT LTM F M Full ll Ye Year ar MSEK 20 2019 19 20 2018 18 201 2019 2018 018 18/19 2018 /19 2018 Group Group, IFR IFRS Net sales 5,996 5,425 10% 18,855 17,206 10% 24,774 23,125 7% Operating profit 832 184 n/a 1,534 982 56% 844 293 n/a Profit before tax 676 78 n/a 1,097 658 67% 332

- 107

n/a Diluted earnings per share, SEK 1.70 0,00 n/a 2.64 1.06 n/a 0.17

- 1.40

n/a Cash and cash equivalents in the parent company 1,565 1,724

- 9%

1,734 Ratos s business ss a area eas, s, R Rato tos' s's s ho holdi lding ¹ ¹⁾ Net sales 5,943 5,071 17% 18,245 16,096 13% 23,671 21,522 10% EBITDA, excluding IFRS 16 ²⁾ 402 231 74% 1,312 1,211 8% 1,400 1,299 8% EBITA, including IFRS 16 331 1,108 1,039 EBITA, excluding IFRS 16 ²⁾ 302 120 n/a 1,016 903 13% 947 834 14% Earnings in the company portfolio ³⁾ 302 127 n/a 1,016 918 11% 943 846 11% Earnings before tax, including IFRS 16 2) 148 568

- 642

Earnings before tax, excluding IFRS 16 2) 173 1 n/a 640 538 19%

- 570

- 671

15% Cash flow from operations

- 65

- 446

n/a 1,203 41 n/a 1,503 341 n/a ¹⁾ Tables in a tinged background are alternative performance measures, refer not 3 Alternative performance measures page 24 for reconciliation. Page 29 contains definitions. ²⁾ Excluding IFRS 16 means that leases are reported according to IFRS standards applicable up to and including 2018. Refer to note 10, page 28 for the effects of the year ³⁾ Reported EBITA excluding IFRS 16, for relevant company portfolio and period. Ch Change % Ch Chan ange % Ch Chan ange %