SLIDE 1

Changing the probability distribution

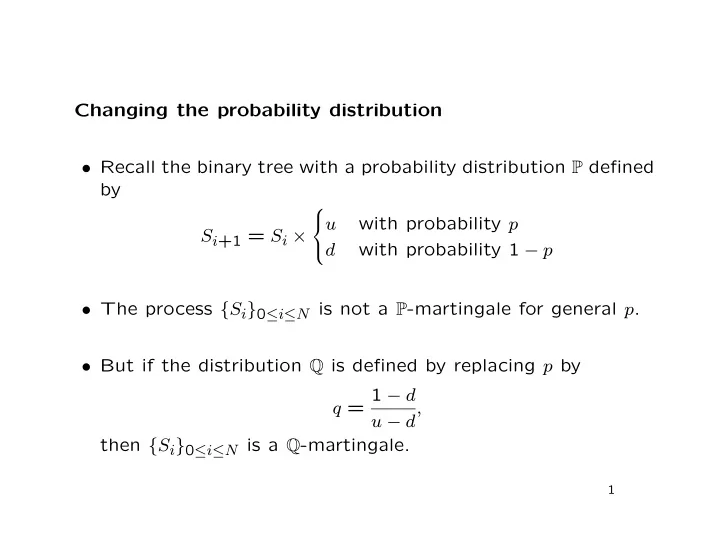

- Recall the binary tree with a probability distribution P defined

by Si+1 = Si ×

u with probability p d with probability 1 − p

- The process {Si}0≤i≤N is not a P-martingale for general p.

- But if the distribution Q is defined by replacing p by