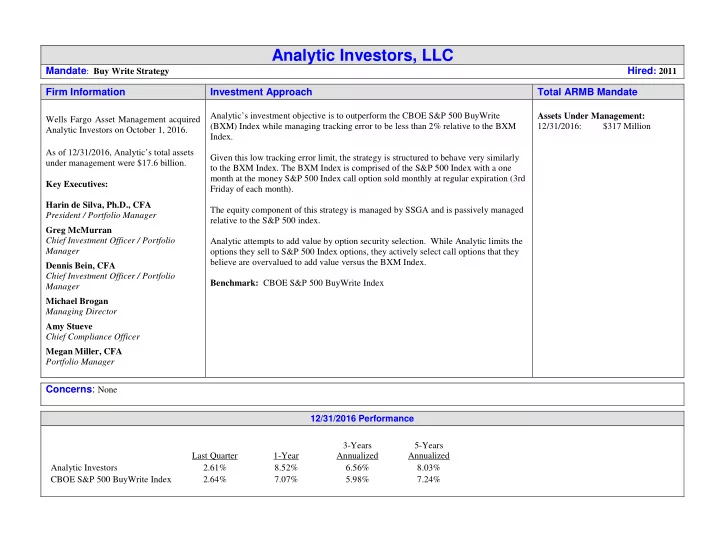

Analytic Investors, LLC

Mandate: Buy Write Strategy

Hired: 2011

Firm Information Investment Approach Total ARMB Mandate

Wells Fargo Asset Management acquired Analytic Investors on October 1, 2016. As of 12/31/2016, Analytic’s total assets under management were $17.6 billion. Key Executives: Harin de Silva, Ph.D., CFA President / Portfolio Manager Greg McMurran Chief Investment Officer / Portfolio Manager Dennis Bein, CFA Chief Investment Officer / Portfolio Manager Michael Brogan Managing Director Amy Stueve Chief Compliance Officer Megan Miller, CFA Portfolio Manager Analytic’s investment objective is to outperform the CBOE S&P 500 BuyWrite (BXM) Index while managing tracking error to be less than 2% relative to the BXM Index. Given this low tracking error limit, the strategy is structured to behave very similarly to the BXM Index. The BXM Index is comprised of the S&P 500 Index with a one month at the money S&P 500 Index call option sold monthly at regular expiration (3rd Friday of each month). The equity component of this strategy is managed by SSGA and is passively managed relative to the S&P 500 index. Analytic attempts to add value by option security selection. While Analytic limits the

- ptions they sell to S&P 500 Index options, they actively select call options that they

believe are overvalued to add value versus the BXM Index. Benchmark: CBOE S&P 500 BuyWrite Index Assets Under Management: 12/31/2016: $317 Million

Concerns: None

12/31/2016 Performance Last Quarter 1-Year 3-Years Annualized 5-Years Annualized Analytic Investors 2.61% 8.52% 6.56% 8.03% CBOE S&P 500 BuyWrite Index 2.64% 7.07% 5.98% 7.24%