SLIDE 1

1

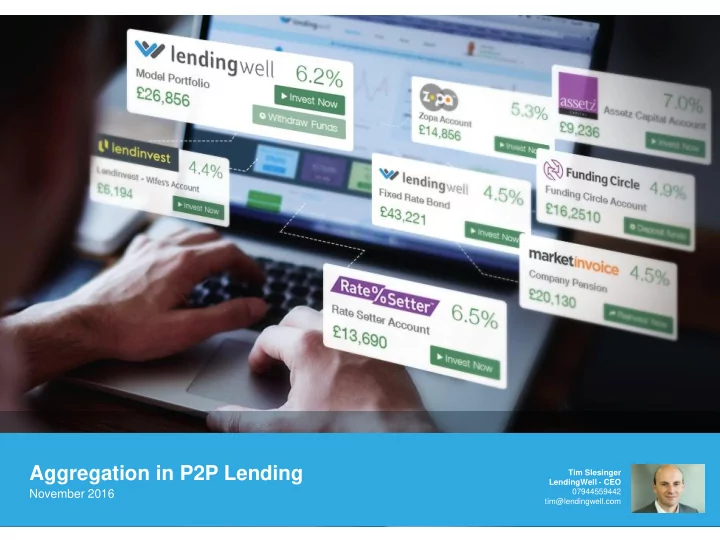

Aggregation in P2P Lending

November 2016

Tim Slesinger LendingWell - CEO 07944559442 tim@lendingwell.com

Aggregation in P2P Lending Tim Slesinger LendingWell - CEO - - PowerPoint PPT Presentation

Aggregation in P2P Lending Tim Slesinger LendingWell - CEO November 2016 07944559442 tim@lendingwell.com 1 UK P2P LENDING MARKET 2.9BN 20BN 53m Expected CAGR 48% 2015-2020 2015 2020 2010 2 AN EVER MORE CHALLENGING LANDSCAPE

1

Aggregation in P2P Lending

November 2016

Tim Slesinger LendingWell - CEO 07944559442 tim@lendingwell.com 2

2010

£53m UK P2P LENDING MARKET

2020

Expected CAGR

48%

2015-2020

£2.9BN

2015

3

95.5% 4.4% 0.1%

Consumer lending Business lending Property lending Invoice financing

2010 <10 P2P Platforms

AN EVER MORE CHALLENGING LANDSCAPE FOR INVESTORS TO NAVIGATE

2016 >100 P2P Platforms

33.1% 23.7% 30.8% 12.4%

4

NUMBER ACCOUNTS GROWTH

11%

TOTAL AuM GROWTH

STILL AN EARLY ADOPTER MARKET…

5

Direct via platforms 1

Investors (Institutional and Retail) invest in loans direct through a lending platform Zopa; Funding Circle; Lending Club

Listed Investment trusts 2

Investors buy shares in an investment trust listed on a stock exchange P2PGI, Ranger Direct Lending, Honeycomb, Funding Circle Trust, Victory Park Speciality Lending

Unlisted GP/ LP funds & Managed accounts 3

Investors invest in an unlisted fund as a limited partner with fund being managed by a general partner Colchis, Ranger Direct Lending, Prospect Capital Mgmt.

P2P aggregators (plumbing solution) 4

Investors put money into a segregated client account with a custodian. The P2P aggregator enables the investors to directly invest in fractional loan parts NSR Invest, Goji, Bondmason, LendingWell

WAYS TO INVEST IN P2P LOANS INCLUDE…

Description Examples

6

CONFUSING!

7

AN EVER MORE CHALLENGING LANDSCAPE FOR INVESTORS TO NAVIGATE

INVESTOR/ ADVISER

DIVERSIFICATION IS NOT STRAIGHT FORWARD

Inefficient Complex Time Consuming

Loan 3 Loan 4 Loan 5 Loan 6 Loan 1 Loan 2

8

underlying loans (property, businesses, car fleets etc.) makes the selection difficult

Source: platforms websites, Altfi Data, World Economic Forum report: “The future of fintech”Which P2P lending platform is right for you?

11.0% 9.0% 7.5% 7.2% 6.9% 5.6% 5.5% 4.8% 3.8% 200 400 600 800 1000 1200 0% 2% 4% 6% 8% 10% 12%

Funding Secure Market Invoice Assetz Lendinvest Funding Circle Lending Works Ratesetter Wellesley & Co Zopa

Net Return - LHS Volume (£m) - RHS

P2P LENDING: ASSET CLASS, RETURNS AND DEPLOYMENT CAPABILITIES

9

investors net of all losses and fees is relatively stable in the 5-6% range.

0.0% 1.0% 2.0% 3.0% 4.0% 5.0% 6.0% 7.0% 8.0% Jul-15 Sep-15 Nov-15 Jan-16 Mar-16 May-16 Jul-16 Market Invoice Zopa RateSetter Funding Circle Overall Sector Return Source: AltFi DataUNLEVERED NET RETURNS IN UK CURRENTLY: 5.4%

10

IF ISA OPEN TO P2P LENDING

£44bn £79bn 2010 2015 2020e

Potential P2P Lending into IF ISA (£bn)

£116bn

TOTAL ISA MARKET

Stock Cash Stock Cash P2P lending

p.a. by 2020

11

FINANCIAL ADVISERS AND ISAS

IN 2015 GROWING 8% YOY

Whole of Market

Independent Research & Reports Training Assets under influence

THE OPPORTUNITY: THE UNTAPPED FINANCIAL ADVISER MARKET

12

Plumbing mechanics; use Burrows chart

Lender 1 Lender 2 Lender 3 Aggregator segregated client A/C Lenders P2P lending platforms Managed by AggregatorAggregator “omnibus” account mgmt: EFFICIENT/FLEXIBLE

Revenue model- EFFICIENT / LOWCOST

Total Expense Ratio

0.40-0.85% Of AuM p.a.

Simple and transparent thin layer of fees charged to lenders only

Aggregators empowered by a ROBUST ECO-SYSTEM Multiple P2P Aggregators emerging in US & UK

NEW ACCESS CHANNEL: EFFICIENCY OF P2P AGGREGATOR

13

OPERATIONAL RISK CREDIT RISK

INVESTMENT RISK

PLATFORM RISK

14

DIVERSIFICATION IS KEY

15

PLATFORM DATA SHEETS

16

DATA-RICH ANALYSIS OF PORTFOLIO

17

A THIRD PARTY VIEW ON AGGREGATORS

18

Next key investment innovation Online Lending? ETN Open Ended Fund... would potentially unlock the Wealth Manager/ IFA market

fund structure

written down or up depending on market conditions)

ratio)

independent index e.g. LARI (AltFi data index)

within 12 months and 100% within 3 years (ETN targets 10% cash equivalents at all times)

investors and later for retail

P2P Aggregator ETN SPV ETN market maker 1 ETN Manager Independent Index provider e.g. AltFi Data

ETN market maker 2 etc Individual Investor 1 Individual Investor 2 Individual Investor 3 Individual Investor 4

THE OPPORTUNITY: INSTITUTIONAL MARKET